Why keeping your "safe job" is a risky financial decision

Most of us probably consider ourselves "lucky" if we get yearly raises. After all, more money is better than less money, right?

Unfortunately, in most cases, that raise isn’t much of a raise at all.

In fact, it may hardly be enough to keep you in the same financial position as you were the year before.

Here’s why.

Inflation gobbles up yearly raises

Inflation is like those sneaking banking fees that are automatically withdrawn from your account. You don’t expect or know about them until we find them in our bank statements.

Inflation is like one giant banking fee that never goes away.

Simply put, inflation is the percentage change in prices from one year to the next. It’s those sneaky price hikes that you don’t necessarily know about unless you pay attention.

Your personal inflation depends on how you spent your money. But unless you had no housing, food or transportation expenses in the last year, your cost of living probably rose at least 2% - and possibly much more.

To paint an accurate picture of whether your finances are improving over time, you need to adjust your salary increase for inflation.

Once inflation is factored in you might find that you’re financially worse off each year even though you received a 2-3% salary increase.

According to the United States Census Bureau, the median salary has increased each year between 0.5% to 4.2% from 2010 to 2017.

During that same period, the Bureau of Labor Statistics reported annual inflation between 1% and 2.2%.

After subtracting the annual inflation from the annual median salary growth, the wage increase is not enough to make up the increased cost of living in most years.

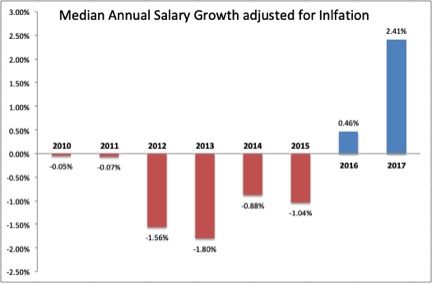

Here’s what the median salary growth looks like after it’s been adjusted for inflation.

Looking at the chart above, it is clear that salaries haven't kept up with rising prices. Each year from 2010 to 2015, we saw a wage loss.

Although salaries increased more than inflation in 2016 and 2017, the cumulative growth from 2010 to 2017 remains in a negative position of 2.5%. That means that over the last 7 years, the median salary lost 2.5%.

In other words, the salary from that “stable” job is barely keeping up with those sneaky increases in costs of living.

With inflation projected to keep increasing at a 2%+ rate each year, buying power will continue to fall.

In the long run, it will become even more difficult for Americans in “safe and stable” jobs to be able to afford their day to day lives let alone buy a home and retire.

Here's an odd truth for many of us:

Safe jobs cost more

To make matters worse, the cost of obtaining these “safe and stable” jobs is on the rise.

According to the National Center for Education Statistics, the average total cost of attendance for a 4-year institution is $104,480 whereas the same degree in 1989 cost half of that amount ($52,892 adjusted for inflation).

Americans are spending more for what is perceived to be “safe and stable” only to end up with a lower standard of living.

Why knowing how much money you’re going to make is risky

Now you might be thinking: "At least I know my salary is going to continue to increase and maybe if I work extra hard my raise will exceed the median salary growth".

That might be true, but the reality of a “safe and stable” job is that salaries are capped. Room for growth will always be limited and predictable.

Although predictability is, to many, a source of comfort, we don’t realize how much it limits our potential for bigger and greater things.

No matter how hard you work, how well you perform, a $60,000 will only grow so much.

Chances are you know exactly where you’ll be financially tomorrow, in one year and even 10 years from now. While knowing that might be perceived as a source of comfort, the downside is you know you’ll probably never make millions or retire early.

That limiting factor, in a way, is extremely financially risky as it prohibits you from ever accomplishing more. You’ll always be “stuck” in the same place financially.

Stable for only a few years

In the 1950s it was normal to get a job and stay with it throughout the course of your life. Americans often made a career at the same company.

But the days of getting a job and keeping it are gone.

According to the Bureau of Labor Statistics, the median number of years employees remain with an employer was 4.2 years in January 2018 down from 4.6 in 2014.

This reinforces the reality that employees aren’t holding jobs anymore.

Not even for 5 years.

A number of factors are at play.

- One of them is the state of the economy. Employees may be forced to leave a job within their first year through no fault of their own due to an economic downturn

- Another reason is that many jobs don’t offer enough growth potential and,

- Staying with the same employer could mean even less salary growth

Regardless, the numbers point towards jobs not being as much of a source of stability and safety as we might think.

Even if you’re changing jobs every 4 years with no periods of unemployment, there is something to be said about why a change is required.

Whether it be due to a lack of fulfillment, lack of happiness, or insufficient wages, the point is, that stability is not really there.

More work, same pay

The earnings of employees overall have lagged behind gains in labor productivity since the 1970s.

On top of that, fewer employees received health or pension benefits in 2015 than they did in 1980.

Part of the problem is our society’s need to always exceed expectations. Companies are under pressure from shareholders, directors and other investors, to continue to beat growth targets or at the very least maintain them.

But when does it all stop? How realistic is it to always do better and more?

Why does that impact employees?

They are under constant pressure to perform better and faster. More is being asked of employees but that additional ask does not proportionally result in additional income.

Let’s be real, paying employees more hurts company targets.

They need to stay as lean as possible. That means there is an incentive to keep few employees, as productive as they can for as little as possible.

Automation rendering us obsolete

To make matters worse, a new study by the McKinsey Global Institute estimates that between 400 million and 800 million of today’s jobs will be automated by 2030.

In the U.S., it seems it’s the middle class that has the most to fear, with office administrators among those who may lose their jobs to technology or see their wages drop to keep them competitive with robots and automated systems.

Here’s the bottom line:

In seeking “stable” jobs, we deny ourselves financial greatness by putting ourselves into molds which prohibit us from reaching our full potential.

Making the decision to pursue a “stable and safe” job is, in that respect, financially risky. Especially given salaries aren’t keeping up with inflation, are not stable and give a lot of us piles of student debt to pay off.

So what’s the solution?

Well, there are a number of ways to making money these days, between side hustles, starting your own business, investing, the opportunities are endless.

To put things into perspective, here’s a real life case from a personal friend. He wished to remain anonymous but for the purpose of illustrating what you could accomplish without a “safe and stable” job, let’s call him Adrian.

As any “good” son would do, Adrian got an education and a stable, well paying, job as an accountant.

It doesn’t get much more safe and stable than accounting.

Even in times of recession, companies still need accountants; there’s just no way around it. On top of that, you career path is well defined to the point of knowing what title you’ll hold and how much you should expect to make.

Long story short, with his education and track record, he was well on his way to clearing a quarter million in 10 years. Not too bad right?

Most of us would be pretty ecstatic to know that in 10 years we’re going to bring in $250,000 a year.

But Adrian wanted more.

He didn’t want to be capped or always know exactly where he’d be, financially.

He didn’t want to be slave to a job that would never give him more than exactly what his career path set out. Let’s face it, you’re not getting paid a quarter of a million dollars to twiddle your thumbs. That kind of money requires consistent sacrifice.

Adrian knew that included long hours and very little time for a family he planned to have.

So, Adrian did what most would consider crazy. With his meager savings, he quit his “safe and stable” job to purchase a failing business for next to nothing.

He had zero experience running a business let alone trying to turn around a virtually bankrupt one.

But he took a leap of faith and promised himself that he would not give up when the going got tough.

He understood there were more opportunities being the boss rather than employee.

Fast forward today, Adrian’s once failed business brings in several million dollars of revenue each month. The best part is, he’s hired people to take care of the day to day operations so it requires little effort on his end.

He continues to look for underperforming businesses and purchases them for pennies on the dollar. He’s added a car part manufacturing company, two estate wineries and about $15 million worth of investment properties to his portfolio.

He could have retired a long time ago, but continues to enjoy flipping failed businesses.

Besides the ability to say when and how much he wants to work, he is truly financially secure.

He chooses to work because he truly enjoys what he does. How many people do you know say they truly enjoy their “safe and stable” jobs and would continue working even if they didn’t need the money and could retire right now?

My guess is not too many.

What was Adrian’s secret?

He understood that a safe and secure job was limiting and he knew that with perseverance, he could learn anything.

He knew that sticking to a safe job was financially riskier as he would never be able to grow to his full potential and would always be limited by a predetermined career path.