Why we're risking a healthcare disaster in early retirement

Trust me, I get it. A healthcare disaster can wipe us out. Healthcare is also super expensive. A major medical procedure can literally ruin people. And, that totally sucks. Knowing how hard a health crisis could punch us squarely in the face, why do we seem so cavalier about the whole thing?

Trust me, I get it. Healthcare can be super expensive. A major medical procedure can literally ruin people. Wipe you completely out, and that totally sucks. Knowing how hard a health crisis could punch us squarely in the face, why do we seem so cavalier about the whole thing?

First, let's get one thing straight: I'm not naive enough to believe that nothing will ever happen to us. Both my wife and I are well aware that things do happen, and we could find ourselves between a rock and a hard-as-hell place at virtually any moment. Trust me, we get it.

But, we aren't letting health concerns stop us from fully realizing our dream of living our lives without the incessant confines of a full-time job. Why are we willing to take such a risk?

Five reasons we're risking a healthcare disaster

Traditional healthcare does not work for us

As full-time travelers, we simply cannot get affordable healthcare through the traditional healthcare marketplace. We don't have the luxury of choosing a primary care physician in a single state because we travel 100% of the time. Typical healthcare plans are rigid and fixed, and our lifestyle requires flexibility that traditional healthcare simply cannot provide for a reasonable price. The healthcare industry fails to deliver for us.

Instead, we're members of Liberty Healthshare.

What is a health share? More or less, you’re sharing the medical costs among those who are generally healthy. Monthly dues are all pooled together and collectively fund the healthcare costs of those who are members of the health share. Health share services are about as straightforward as anything I’ve seen in the healthcare industry, and a slew of full-time travelers use Liberty (including Michelle from Making Sense of Cents).

Liberty HealthShare happens to be a non-profit organization, which means revenue is not the predominant factor in health services for its members. However, they aren’t required to cover medical expenses either because they aren't subject to the incomprehensibly monumental collection of healthcare-related rules and regulations of traditional health insurers.

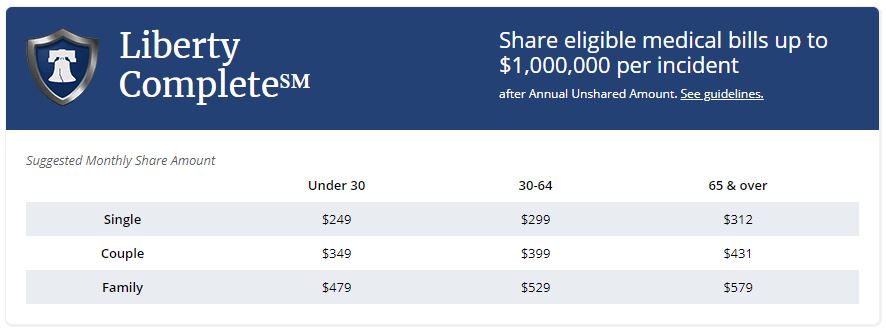

We signed up for Liberty’s “Complete” service account, which covers 100% of eligible healthcare costs up to $1,000,000.

As a couple, we pay $399 / month for service on both of us. We also paid a $135 signup fee upon acceptance into the program. The plan requires a $1,000 Annual Unshared Amount, which is Liberty’s way of describing out-of-pocket expenses.

There is no such thing as “in-network” doctors with health shares. For our $399 / month, we can go to any doctor at any hospital in any state – a requirement for those of us who travel full-time.

While health sharing services can be quite a bit cheaper and more flexible than traditional insurance plans, they also aren’t governed by the same laws that insurance companies operate under. This means that health shares are under no legal obligation to cover your medical costs.

In addition, most require their members to abide by certain ethical rules – such as no smoking or excessive drinking, etc. And if you’re skydiving and hurt yourself, they probably won’t cover those types of expenses. If you are engaging in selective activity that increases your chances of huge healthcare costs, health shares may not cover you. It's how they're able to keep costs much lower than traditional insurance.

Including pre-existing conditions. My wife suffers from migraines, which is a pre-existing condition. Liberty HealthShare will not cover migraine-specific treatment for the first year. While not ideal, I can at least appreciate the fact that we know that up front - and, Courtney has figured out what causes her migraines, too, and altered her diet to largely prevent the worst of them.

Health shares aren’t required to accept you. If you are overweight or lead an unhealthy lifestyle, you may not be a candidate for membership. That’s just the way it is, and it helps to keep costs down for all members.

It may not work for everybody, but it works for us.

Check out their “Do I Qualify?” page for more on how Liberty runs their ethical rules and system of beliefs.

We are young and healthy

Basically, we are hedging our bets at the moment. We have no kids to worry about, and both my wife and I are young (mid-30s), healthy and feeling great. While we both recognize that there are no guarantees in life and that anything can happen, we also believe that history is a pretty good predictor of the future.

At least, the immediate future.

The fact is neither of us has a history of health-related problems. I have asthma and my wife suffers from migraines, but through a systematic change in our diet and lifestyle, we are both able to stave off most of what's ailed us in our lives.

For example, mold kicks my ass. We spent some time around the Florance, Oregon area last year along the Pacific Coast Highway. Our Airstream was parked underneath a dense canopy of trees. Everything was damp. That wetness caused mold to practically hover in the air, and I had to use an inhaler almost every night before going to bed. It was horrible. But, we know what causes my asthma to flare up, and we now avoid places that might spur respiratory problems for me.

My wife's migraines are caused primarily by histamines, and she's voluntarily changed her diet in a hugely significant way - eliminating gluten, dairy, and most meats. She only eats foods that she knows to play nice with her histamine intolerance. This includes cutting out some foods that she previously loved. This isn't something that a lot of people would do.

But, it is something that WE do. She hasn't had a migraine in well over a year, so her need for expensive medications is almost non-existent.

We're flexible to the extreme. More on this later in this post.

We are risk tolerant

My wife and I are on the more risk-tolerant side of early retirement. We quit our jobs at 33 and 35, respectively, with around a million in the bank.

But regardless of our personal situation, I believe taking risks is smart. Risks put us in a position that forces us to remain vigilant rather than complacent. Risks help us to understand the world around us and accept the fact that things might not go right.

One of those “what ifs” might come true.

And, that’s okay. It’s a risk. But, we are all different. Some of us are more accepting of risks than others. Many of us believe that the opportunities in early retirement are worth the risk of calling it quits without several million in the bank. Depending on our lifestyles, we may not need several million sitting there, waiting.

Some do. Some don’t.

And there’s absolutely nothing wrong with being risk-averse, either. I think there’s wisdom in working longer to pad your stash a bit more, which will make it easier to withstand a variety of market conditions, inflation, and health.

Two ways to think about early retirement:

More risk-averse: “It’s true that I don’t know how much I will need, so I might as well work a bit longer to make sure I have enough to live comfortably as well as pay for unexpected expenses.”

More risk-tolerant: “It’s true that I don’t know how much I will need, but flexibility in retirement, along with opportunities to make money, is enough for me. I’d rather not continue working a job I don’t like for money that I may not need.”

Different strokes for different folks.

For us, taking on risks don't bother us, and that's based on our life histories and observable environmental conditions. The odds appear to be in our favor.

We are willing to travel for our health

Though not an ideal solution, we are also willing to travel for our healthcare needs, especially with preventative care and medications. In fact, we take a family vacation to Mexico every other year and we take the opportunity to purchase medications for a fraction of their cost in the U.S. My asthma medication costs around $7 USD in Mexico. In the United States, it's easily 10x more due to the mountains of bureaucracy, regulation and doctors visits that are required.

We're also entertaining the possibility of living for extended periods of time overseas where costs are much lower than in the United States - including healthcare. Jason Fieber from Mr. Free at 33 wrote about his experience visiting a hospital in Thailand. How refreshing! :)

In the end, we're ready and willing to go where ever we have to to get the very best care at the very best price.

We are motivated enough to change our habits

I alluded to this before, but both my wife and I are flexible and determined enough to change the way that we live our lives so it works best for our health. My wife has streamlined her diet so it plays nicely with her histamine issues, including cutting out foods that she otherwise loves - like Spinach, which is high is histamines.

I can't do mold, so we'll never stay for extended periods of time around wetter areas of the country (like the Oregon coast).

We've also altered the way that we travel. During our summer travels last year, I never set foot in the gym once. Instead, we hiked and biked for exercise. But still, that wasn't quite enough for me. I put on 10 to 15 pounds during the summer because I tend to burn a hell of a lot more calories when I do resistance-type training - not cardio like hiking. I also enjoy resistance training way more than cardio. I find cardio exceedingly boring and high impact.

For resistance-type of work, I need a gym. This year, I bought a nationwide Planet Fitness membership and we're prioritizing our camping locations around gym locations.

In fact, we're hangin' out in Santa Fe, New Mexico at the moment - they have two Planet Fitness gym locations in town, so I'm going to the gym every day. And, their nationwide membership lets each member bring a guest. Guess who my guest is? ;)

When there aren't Planet Fitness gyms, I ask for a week pass at any local gym that has the weight and equipment that I need for a decent workout (I did this in Taos, NM at Deliberately Fit). We also pay for this privilege, and that is okay. I know how I stay healthy, and even when living a life on the road, I'm not going to fight it.

I tried to fight it last year, and it won. This year, I'm not. Our travel habits have changed in order to prioritize our health the very best that we can to reduce the chances of problems resulting from poor health.

Once again, I know this won't work for everyone, but it works for us. We love seeing this country and experiencing everything it has to offer. Today, we're leaving the Great Sand Dunes National Park area for points North. After my morning coffee, of course.

That's it, folks! We fully realize that our current living situation is a bit of a risk from a healthcare perspective, but history doesn't lie. We know what works for us. We know how we stay healthy and lean. There is no guarantee that we'll remain healthy, but prioritizing our health in a big way through life will increase our chances of staying healthy.

For now, it's well worth the risk.