Should I retire early? Here are 4 steps to make it happen

Ever asked yourself should I retire early? If the answer is yes, then you're not alone. A lot of us want to, but that doesn't mean it's smart.

Have you ever asked yourself should I retire early? If so, you're not alone. A lot of us want to, but just because we want to doesn't necessarily mean that we should.

Unless you want life (reality?) to kick you squarely in the face, early retirement isn't something that you just "wing", at least completely. Your ducks don't have to be completely straight, but they must be lined up in a way that at least loosely resembles a row.

Stand 'em up. Situated them, then pick them up when they fall.

Early retirement isn't "hard", necessarily. But, it can be fickle. Things will change all the time, so don't feel like you'll need every last detail covered. That's a fool's errand. Instead, keep your strategy tightly focused on your lifestyle, but high-level enough to morph and change as required.

I'm a 36-year-old early retiree, and here's what I've learned about building a simple, but ridiculously effective, early retirement strategy.

Should I retire early? Here's how to build your early retirement strategy

This stuff isn't rocket science, but it does take some time to figure out if the answer to "should I retire early: is yes. Experimentation, even. Not all of us get it right on the first try, either. And, that's okay. Nobody is perfect.

Don't expect perfection. Perfection is never the answer.

Building your retirement strategy comes down to four primary topics:

- Access to liquid financial resources (yes, money!)

- Avoid going broke paying for healthcare

- Understand your purpose in life outside of a full-time job, and

- Assess your ideal lifestyle after peacing out

Below, we'll detail each one in turn. Let's go!

You have money, but how will you access it?

Money is great, but if it's locked up in some inaccessible caldron of laws and legalese (ie: your 401k or IRA), then accessing that money before you're ripe enough to retire traditionally might not be possible - at least not without penalties.

Most people have their money in a variety of places, including:

- Bank (checking) accounts

- Savings or money market accounts

- Brokerage accounts

- Retirement accounts (ie: 401k, 403b, Roth IRA, etc)

Money in your checking account is the most liquid - meaning, you can run your fingers over those beautiful greenbacks at a moment's notice. It's instantly available. However, you also aren't building your wealth through the power of compounding interest by stashing your money in a checking account. That's the major downside.

Savings and money market accounts are a great way to keep liquid assets that build - albeit much slower than in the stock market. My wife and I use Ally's relatively high-interest rate savings account to make some money on nearly four years of living expenses that we have stashed there. Money in savings or money market accounts is relatively easy to access.

A Brokerage account is a wonderful option to increase your investment portfolio beyond what you might be saving through your company-sponsored retirement plan. We use a Vanguard Brokerage Account to hold a good portion of our net worth in the market.

Retirement accounts are long-term investments in the market that cannot be accessed before turning 59 and 1/2 without penalties - with a couple of exceptions.

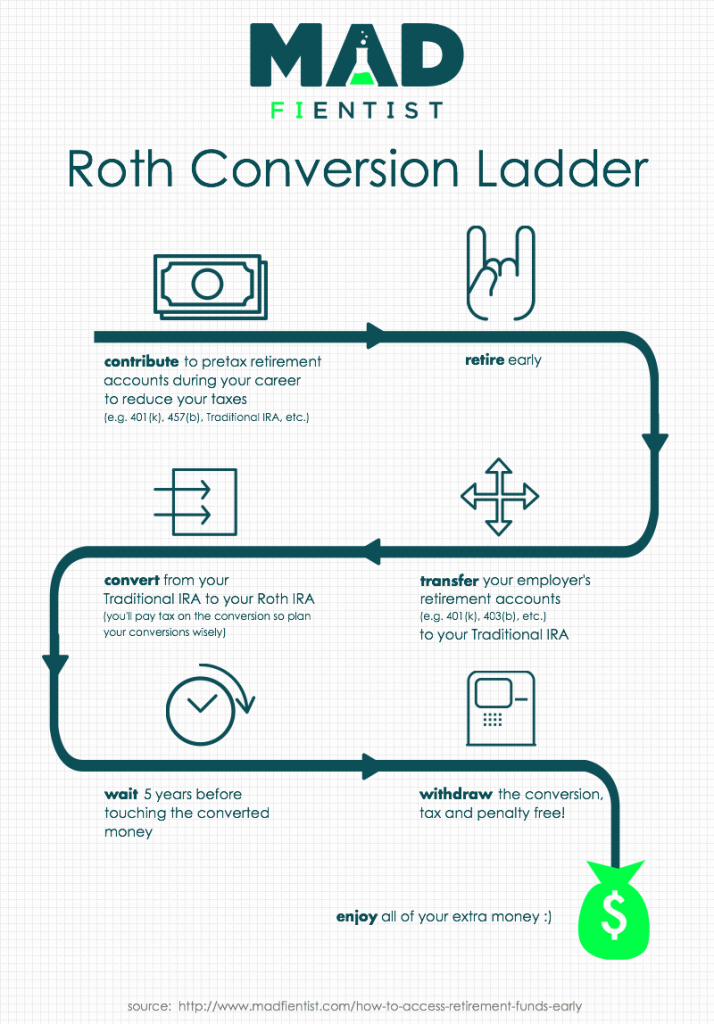

There are ways to get at your Roth IRA before cresting the 59 and 1/2 age mark, and that's the Roth conversion latter. The Mad FIentist wrote a concise but very detailed summary of how it all works, along with this sweet infographic:

Details regarding the Roth conversion ladder is well beyond the scope of this article, but I highly encourage you to check out Mad FIentist's article on the subject. After all, he doesn't call himself the "Mad FIentist" for nothing.

In retirement, we need liquid cash to spend. This might come from capital gains through stock market investments, or real estate income, pensions or anything else (including side hustles). If you're younger than 59 and 1/2, you won't be able to rely on your long-term retirement savings to fund your lifestyle (aside from the Roth hack above). Income from other sources will be required.

Easily-accessible income, that is.

What are you doing about healthcare?

By far, the question of healthcare is the most common I get.

And, I completely understand the concern. It's a huge cluster. And unfortunately, healthcare costs are monumental in the United States - so high that they are driving many retirees (especially early retirees) out of the country. We aren't at that point yet, but living and/or seeking healthcare abroad is an option that we'd consider.

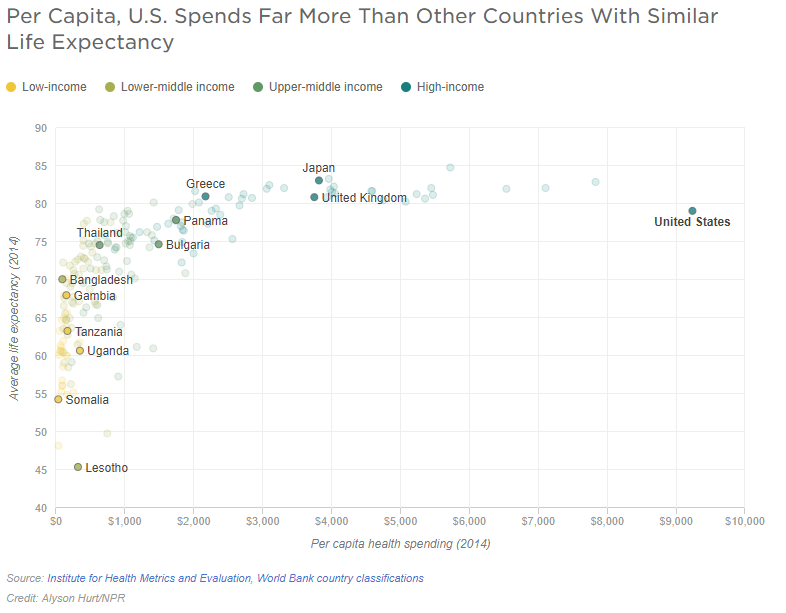

After all, the United States easily leads the world in healthcare spending per capita, as the following graphic from NPR clearly illustrates. Sadly, the high cost of healthcare doesn't mean our life expectancy is any greater than nations who only spend a fraction of what we spend.

As of 2014, both Japan and the United Kingdom have a higher life expectancy than those living in the United States, and Thailand only trails the United States by five years - but, their health system is very sophisticated without the spending.

Clearly, healthcare spending is a huge problem in the United States, and the politics that govern the problem is a huge mess and tend to only make healthcare costs more expensive. If your plan is to live out the rest of your life in the United States, healthcare will be a primary concern.

Military retirees won't need to worry about healthcare as much as the rest of us because health coverage is built into their 20-year retirement benefits. Others may have healthcare options, even after retirement, from their long-standing employment history through their former companies. But for the rest of us, this mess needs to be figured out.

The relatively new healthcare marketplace (Healthcare.gov) designed as part of the "Affordable Care Act" provides healthcare subsidies for those with low incomes - typical of an early retiree. Many early retirees take advantage of these subsidies even though their net worth might be extremely high. According to the law, this is 100% legal and, if I were offered a subsidy, I would probably take it as well.

To make matters more complicated, a travel-based RV lifestyle is becoming much more popular, and traditional healthcare providers won't cover full-time travelers - and those that do often only do so after a steep increase in insurance premiums. As an early retiree, the costs associated with a traditional insurance plan that doesn't require a stationary primary care physician is much too expensive. I'd have to go back to work.

This is where health shares come into play.

Health share programs have become extremely popular in the RVing community. When you need the freedom and flexibility to see any doctor at any time (common among full-time travelers), regardless of where you are in the United States, health shares fill the need nicely. They provide health reimbursements at a fraction of the cost of a traditional insurance plan.

You are treated as a cash paying patient, and legally, health shares are under no obligation to cover your health expenses (especially for elective surgeries or anything that results from behavior that the health share does not condone (ie: smoking, skydiving, etc)). Many also won't cover preexisting conditions, at least for the first several years. Even with these limitations, a health share program might still be right for you.

Health shares are NOT "health insurance", and quite frankly, that's a part of what attracts us to this option. Less expensive. More streamlined. Easier to understand.

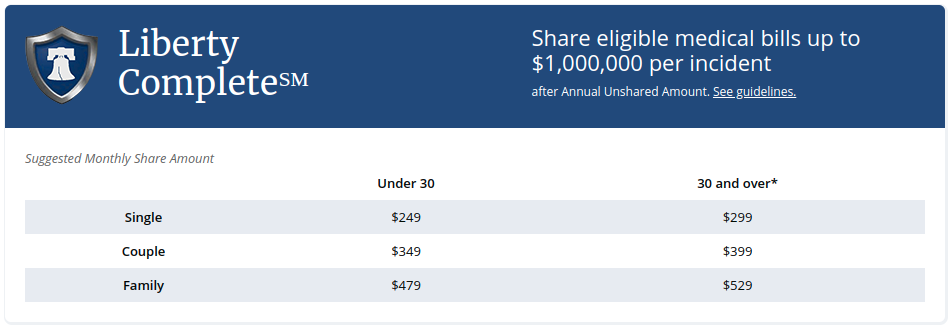

For the record, we use Liberty Health Share - one of the most popular options in the full-time RVing community. We pay $399/month combined for my wife and me. We have the $1m plan.

Once your healthcare is figured out (arguably the toughest part of this equation!), everything else becomes much easier.

Should I retire early? Well, what's your purpose in life without a full-time job?

Retiring from full-time work is great, but doing so opens up each and every day to do pretty much whatever we want. That sounds great to a lot of people, but those who derive their happiness entirely from their careers might have a tougher time feeling productive and accomplished after calling it quits from full-time work.

What happens when you've got the entire day to fill? You might be okay for the first couple of weeks. Even a couple months. But eventually, early retirement becomes the new normal. The excitement of quitting work wears off and you're left with actually managing your life around your new "normal".

Should I retire early? Well, what's going to fill your day?

Part of our purpose is travel. Here's a shot of our Airstream parked out in the Colorado countryside in May 2018:

If you're a retired home-builder, you might volunteer with Habitat for Humanity. If you spent your career sitting in front of a computer, you might begin building IT widgets for yourself rather than a faceless company. Or your neighbor. Or family. Woodworkers might build mantels or tables for friends.

In whatever way that you spent your career, your post-career lifestyle needs to be filled with something. Don't retire from being productive. If there is nothing meaningful that fills your life outside of work, then don't retire until you find it.

Let's summon the wisdom of Dr. Hinohara

Last year, 105-year-old Dr. Hinohara died after making a life-long and significant impact on Japanese healthcare. Particularly, he studied longevity. In other words, what makes us humans live longer?

In 2009, he spilled the most critical elements of living a happy and healthy life to Japan Times, and it’s incredible how similar his findings are with the bulk of the early retirement community.

And, it’s these findings – and, in general, a focus on living a happy and productive life post-retirement, that is most important in life longevity.

Energy comes from feeling good, not from eating well or sleeping a lot.

In other words, don’t focus too heavily on what you should be doing. This doesn’t mean we should purposely deprive ourselves of sleep. Naturally, that’s stupid. Instead, focus on how you feel and do what feels natural to you. These insipid one-size-fits-all standards and procedures won’t necessarily work well for everyone.

All people who live long — regardless of nationality, race or gender — share one thing in common: None are overweight.

For breakfast every day, Hinohara drank a cup of Joe, a glass of milk and some orange juice with a tablespoon of olive oil in it. Believe it or not, lunch consisted many times of milk and cookies (when he ate lunch), and dinner was primarily veggies, fish, and rice – with the occasional cut of lean meat.

I’m pretty darn close to this, though I’d love to start trying that milk and cookies lunch regimen. Breakfast for me is nothing but a cup of coffee before I hit the gym. Lunch is generally a leftover from the night before, which generally consists of lots of veggies in a homemade sauce. Sometimes, meat. Lots of cauliflower, too. Sometimes, we’ll exchange rice with cauliflower rice. Dinner is the same as lunch because my lunches are dinner’s leftovers. ?

Always plan ahead.

Okay, I totally suck at this part, though my wife more than makes up for my shortcomings in this area. I fly by the seat of my pants, free-wheelin’ it as far as momentum will take me. I do admit that I could proooooobably use better planning skills, but that’s why our marriage works so damn well. She picks up the slack where I leave a lot to be desired.

There is no need to ever retire, but if one must, it should be a lot later than 65.

Wait, what? Never retire?

No, that’s not what Dr. Hinohara means. What I believe he means is…never retire from being productive regardless of whether or not that productivity originates in a traditional office or from a full-time job. We need a purpose in our life, and if you can find genuine purpose without holding down a full-time job, then you’re very much like me. And my wife. Our jobs were critical during the accumulation phase of our life, but now we’re on to the next phase.

Share what you know.

Hmm…I try to do that on the blog and through discussion forums. I also did a question and answer post as well as spilled the beans in an FAQ.

Don’t be crazy about amassing material things.

Got that one covered. Like a blanket over a tennis ball. Like, hard-core covered to the extreme. My wife and I sold both of our homes and about 90% of our worldly possessions and bought a 30′ Airstream, named Charlie, in which we travel the country.

We live in 200 square feet and it’s plenty of space for both of us to feel productive and happy. Neither of us cares about material possessions any longer. Should I retire early? Yep, for us it made sense.

Life is filled with incidents.

I love this one the most. Life is nothing but an endless series of situations. Of experiences. We generally go from one to the next without a passing thought. But, maybe we should think more about these “incidents”. Enjoy as much as we can the situation that we’re in. After all, don’t we early retirees clamor on and on about experiences rather than things?

Yup, because there’s incredible wisdom in that philosophy. Slow down, take stock of each incident and enjoy whatever it is you’re experiencing in life. If you can’t enjoy it, do something else.

Find a role model and aim to achieve even more than they could ever do.

I’ve had several role models in life, and each time, I wanted to achieve at least as much as that person did. Though I never outwardly acknowledged a desire to outdo that other person, achieving a level of happiness that is on-par was always my goal. I understood that not everything will turn out the same way, even if I did everything in exactly the same fashion. Our lives are not made up of repeatable binary code. Shit doesn’t work that way.

Is your lifestyle actually realistic?

Lastly, let's discuss the meat of early retirement: Your lifestyle. The cost of your lifestyle cannot exceed the depth of your financial resources. For example, if you loved to travel to exotic tropical locations for $10,000 a pop while you worked full-time, that same style of travel may not be possible without your former income.

The cost of your lifestyle cannot exceed the depth of your financial resources

The sticking question is simple: How much money does one need before giving one's career the finger? As with most questions, the answer depends.

If you're into LeanFIRE (like us), you may not need quite as much money. After calculating your yearly expenses, using the 4% rule as your foundation can provide a good ballpark for this answer. For example, spending $40,000 a year requires around $1,000,000 in net worth if you're using the 4% foundation. Adjust up or down as necessary.

FatFIRE folks want to spend a lot more after calling it quits and, as a result, will need to amass quite a bit more resources before quitting.

...that, or design and build sources of side income that can provide cash flow. Side hustles like consulting, social media management, pet sitting and all kinds of different activities can help provide cash flow after throwing in the career towel.

So, should I retire early?

The larger idea behind this point is simple: One's lifestyle needs to be designed in proportion to one's financial position. You can't live like a king or queen in retirement without the resources to provide for it. You'll find yourself back at work in short order!

Be realistic and confident as you're figuring out what the hell you'll do after calling it quits. If you can't see yourself living without cable television, or expensive restaurant meals or even that weekly indulgence in high-priced booze, then take those expenses into account while you're swimmin' in cold hard income from your full-time job.

And, that's really it. Once you've figured out how you'll access your money (penalty-free!), manage your healthcare, find your purpose and design an appropriate post-retirement lifestyle, everything else falls into place much easier.

This is how to turn the answer to "should I retire early" to yes, yes you should. :)