Escaping the debt spiral: A high income path to financial independence

Debts are big business in the U.S. Escape the debt spiral by using these seven proven techniques to keep your money safe and under control.

In the United States, the debt spiral is as common as a BMW in a wealthy neighborhood, or like Corollas on a normal street.

Throughout all income levels, debt puts people into a position of weakness by owing money to banks and collection agencies, and the more debt we take on, the easier it gets to accept. It really is something of a "spiral".

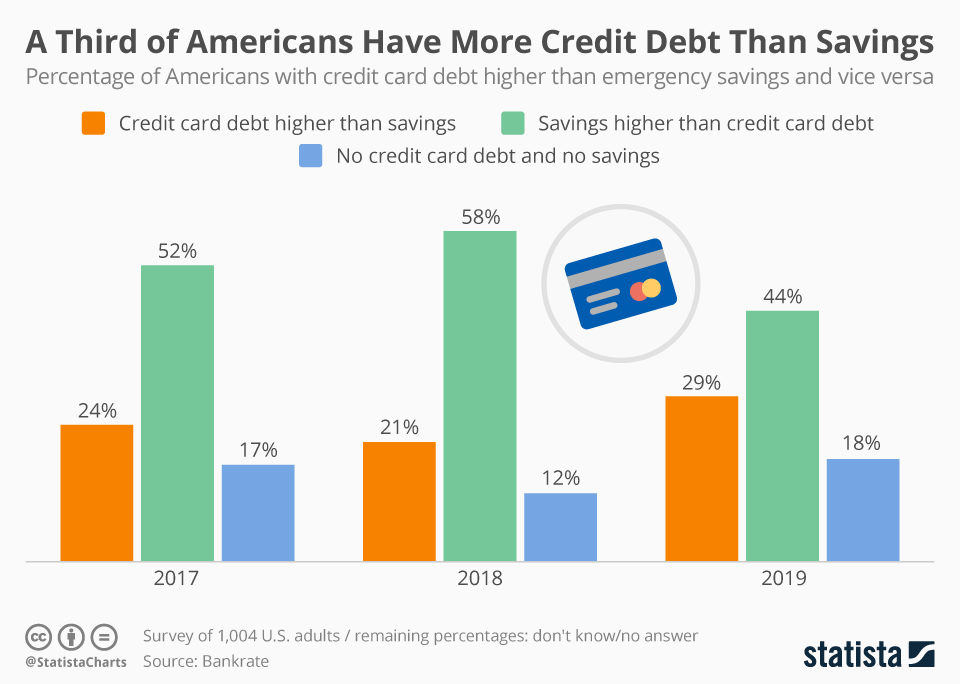

And, here's a particularly devastating statistic: A third of Americans have more in credit card debt than they do in savings. Whoa, Nelly.

Houston, there's a huge problem here.

But, here's the bigger problem. It doesn't just affect "low income" people.

Just because you're gainfully employed and earning good money doesn't mean that you're in the clear. In fact, high-income debt is a thing. It plagues a LOT of people who earn big money and operate within a culture where spending money isn't just accepted but encouraged.

In fact, the more money that we make the more we think we can spend. It actually gets worse for many of us. Each raise cycle. Every bonus. The numbers show that too many people spend the large majority of what they bring in.

That's not how wealth is built, and that's definitely not how retirement happens.

Joe Stanley was on this very same path. Together with his wife, they earn over $100,000 a year as federal employees and quickly fell into a lifestyle of save-the-minimum and spend the rest.

Just like I did.

In this article, Joe outlines their story, early struggles with debt, and how they’re working to achieve high-income FI with useful tips to control spending, enjoy life, and build wealth.

At the bottom of the article, be sure to read Joe's seven actionable steps to build wealth rather than spend it - and retire on your terms.

We Are High-Income DINKs

Before I dig into how we’re approaching our path to FI now, it’s worth giving a bit of background about myself and my spouse.

We have been married just over 10 years (right out of college) and have spent all that time as a dual income no kids household.

That's right, we are total DINKs.

My wife and I (Mrs. and Mr. FedFire) both have PhDs but did all of our grad school work while working full-time jobs. We’ve been DINKing our way along for about 10 years as full-time working professionals and full-time grad students.

I’m an engineer and have worked with the Federal Government for my entire career, while Mrs. FedFire has enjoyed a career as a public school teacher.

In case you're wondering, federal workers make pretty decent wages.

Our Income Over Time

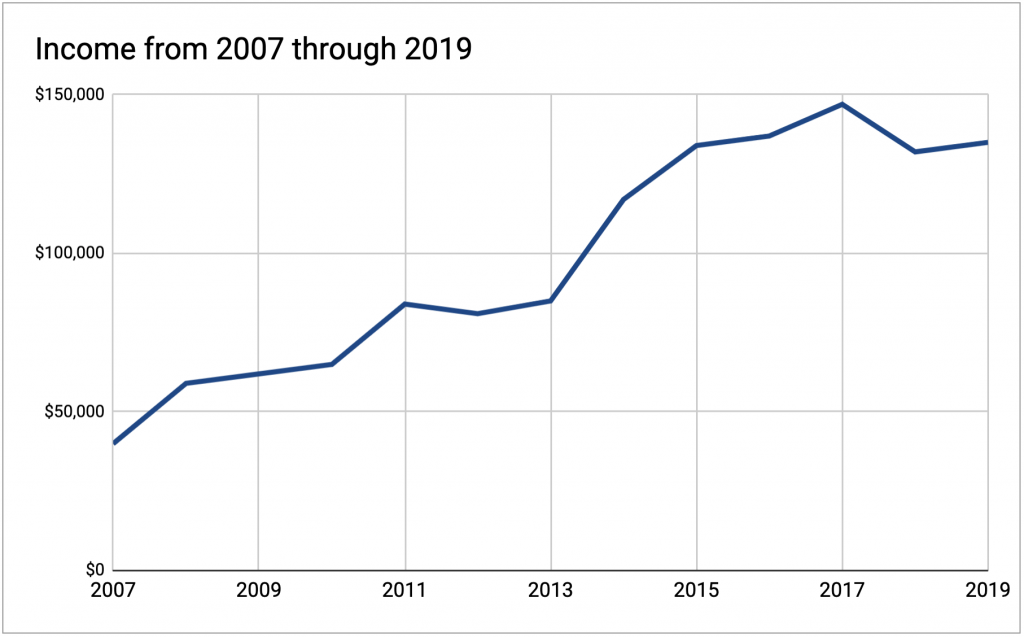

When I first started as a Fed, I had several mentors tell me that my salary would increase quickly early on, but after that, it will hit a plateau.

11 years later I can attest to the truth in that statement. Mrs. FedFire had a slower progression, moving across and down a set public school pay structure. Even so, our combined income now is more than three times higher than when we started working about 11 years ago.

In 2017, our household income peaked around $150K, putting us somewhere in the 80-85th percentile in the US. For a number of reasons that has dropped back to about $135K, but our current situation gets us free housing and also includes a sizeable chunk of tax-free income, so our bottom line is pretty much unchanged.

Managing an Increasing Income

It’s not hard to find stories about the recent med school or law school grad with a new degree and a mountain of debt in hand, thrust into a high paying job and immediately living up to or beyond his or her means. Though we didn’t experience quite this step-change in income, we have had a steady and substantial increase.

Early on this led to some pretty poor choices.

We have lived in a low cost of living area, so the $60K we brought home our first year of marriage felt like a lot of money. We hit the 5% employer match for my Thrift Savings Plan (the Federal employee 401K), put about $1,000 each into IRAs, and spent the rest.

Two years later we still had about $20K in student debt and had made a number of poor financial decisions.

For example:

- in our garage were two financed cars,

- our bedroom was furnished on a 0% intro credit card, and

- we had made numerous other large purchases on credit

We were buying all that stuff to fill the 4 bedroom house we had just moved into. How big is too big when it comes to homeownership?

After three years in, we had already bought and sold a condo, moved into a house that cost twice as much and had about $60K worth of stuff on credit and $20K in student loans.

It was spiraling fast!

How the Debt Spiral Happens

We were focused on our income and how much we could spend. There was a bottom line coming in, and that made it much easier to spend a whole ton of money. Whether it was for debt payments or groceries, it all came back to the bottom line.

I had myself convinced that saving 5% to my TSP plus some into IRAs would have us set for the future. After that, every penny that came in could go out.

No problems. Budgets? Hah! I have this thing figured out.

All of this credit was zero or very low percent financing. We paid off the amounts on 0% intro rates before we ever accrued interest. In my mind this was prudent money management: we were getting FREE MONEY, we’d be stupid not to take it!

But the money wasn’t free, and living a life built on debt was stupid.

We continued to make those payments and acquire more stuff, but we were doing almost nothing to save for the future. We didn’t have crippling debt, but we also weren’t building wealth.

All of this was happening during one of the worst economies in history.

Looking back, our risk was stupidly high. Either of us could have easily lost our public sector job; if that happened we wouldn’t be able to pay the debt and would have quickly lost control.

The Debt Spiral Stopped Making us Happy

We realized our spending started to have diminishing returns of happiness.

In early 2011, I learned of an opportunity for a one-year assignment overseas beginning in 18 months. It was something we really wanted to do, but it meant Mrs. FedFire would have to take a year off work.

With very little savings, this presented a powerful issue.

Becoming a one income household was something we couldn’t sustain. Our spending and debt accumulation put us in a spot where slashing our income prevented us from taking this opportunity due to our costly lifestyle.

I would still make $65K, but that wouldn’t even cover our expenses.

That was ridiculous.

Our spending had gotten us to a place with no flexibility! That’s a diminishing return.

We knew we wanted to do this, so we buckled down and started paying our consumer debt as fast as we could. We had a timeline and a target: 18 months to clear the consumer debt.

In the end we didn’t quite get rid of all of it, but we got darn close. The last hurrah was selling one of the financed cars at just enough to cover the loan value; it’s humbling to calculate out how much you’ve spent on a car loan and realize at the end you have nothing to show for it!

The Path to Responsible Savings, Wealth Building, and Financial Independence

How did we go from a debt spiral of monthly payments to planning for FIRE at 43?

We haven’t increased our spending since the beginning of 2013.

Meanwhile, our income has increased from $80K to $135K. During that time, every salary increase has been put straight into savings.

Using this strategy, we’ve increased our annual retirement savings from $6,000 in 2012 to $65,000 for 2019.

Halfway through 2019, we’ve saved $35,530, so we’re ahead of our goal so far. We do this by living on roughly $4500/month of expendable income. That’s still a good chunk of money and lets us travel, eat out, go to shows, and enjoy ourselves.

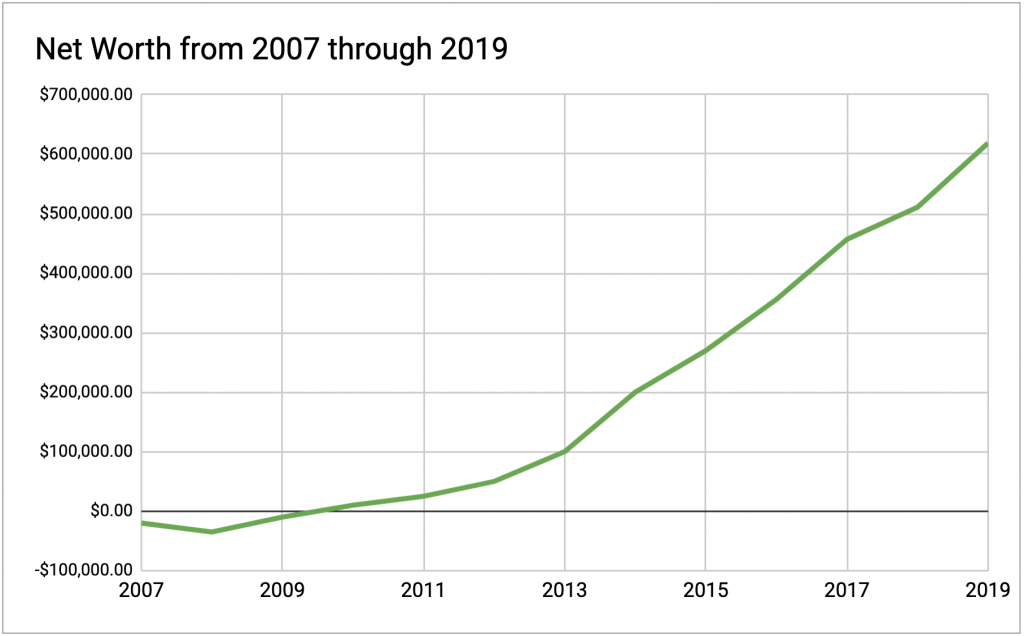

Our net worth has also skyrocketed during this time and we’re on the path to hit our FI-goal ($1.75M in investable assets) at age 43/44.

The growth in our net worth has not been an accident. We have been intentional about saving, limiting our spending, and investing in simple index-based funds.

We have, of course, been fortunate to be riding the current strong economy, but as they say: make hay when the sun is shining.

7 Actionable Approaches to FI for High-Income Earners

Now for some specific things that we have done to make this change. Many of these aren’t specific to high-income earners, but I do think they highlight the traps that high-income earners fall into. These traps lead to spending getting in the way of prudent saving.

1: Understand your goals and build a strategy

It doesn’t matter if you want to retire at 43 or 63, having a goal is critical. It allows you to build a strategy and a plan for getting there. Think about not only what your goals are, but why they are your goals. This can give you the motivation needed to get to work. I wrote about our plan here.

Investment Policy Statement

Once you have savings goals set, make an IPS to outline how you’re going to invest and help remove emotion from the process. Read all about it here.

Tax Planning

Understand the basics of the tax code and how it affects your money. If this is too much for you, find an independent financial planner who can help you. As part of that planning, use a tool to estimate your future tax bracket, which can inform whether to favor pre-tax or Roth contributions and how raises may affect your marginal rate. Simple changes to where and how you save can result in putting away thousands more toward retirement each year.

2: Reckon with the diminishing return of happiness

There’s no easy way to find your sweet spot in terms of how much to save and how much to spend. Planning can help, but it’s easy to put something in a plan that seems achievable and have it turn out to be hard. You will likely need to fiddle with savings rates early on. If you use automation (see tip 3), you adjust your savings until you find the spot where you’re comfortable.

Our approach to this was to set a hard limit that was quite a bit lower than our spending had been and force ourselves into it. That limit moved up a bit at first, but within the first year we had settled on a spot that was working for us and have been there since.

3: Use automation

All our retirement savings goes directly to either Vanguard or the TSP with the “pay yourself first” approach. The remaining money goes to a checking account at a local bank covers our expenses. If the checking account tops $10,000, I transfer $2,000 to Vanguard and we increase our savings for the year.

Automating all of this is key because it grounds our frame of reference on spending to what we actually have available after all hitting our retirement targets. If your employer offers auto-deductions, use them!

4: Don’t think about anything in terms of payments

The minute you fall into the trap of thinking about purchases in terms of payments, you start the debt spiral. There is a reason lenders explain everything in terms of payments: it’s far easier to see yourself paying $1,000 per month instead of the reality of spending $60,000 on a loan for a car that costs $50,000 and will depreciate to $40,000 the minute you drive it off the lot. Don’t fall into the marketing trap of thinking about life in payments - it’s really hard to get out.

5: Make big purchases in cash

It’s the same mentality as “pay yourself first” with savings. If you have a plan for big purchases (home renovation, car, etc.), start to set aside savings now for that purchase. When the time comes, buy it with cash. Buy with cash to avoid the risk associated with debt payments, increase your flexibility, and allow you to control your money.

6: Track your goals

Tracking net worth, income, and expenses is hugely valuable: seeing your net-worth increase can be a great motivator. Whether you choose Personal Capital, Quicken, Mint, or something else, the important thing is: you need to know what you have in order to manage it appropriately. Using these tracking tools is also a good way to address tip 2.

Track expenditures to understand where you are and use that to help set goals.

7: Keep investing simple

The more complicated you make your savings and investment strategy, the more likely you are to deviate from it. I use the Boglehead approach to investing for all our investable assets. There are other options out there, but the bottom line is: just because you earn and save at a “high” level does NOT mean your investments have to be complicated!

Be Intentional

This is by no means an exhaustive “how-to” list, but it’s a summary of some of the biggest things that have helped us along the way.

As is often written about in the PF community, a lot of this comes down to intentionality in decision making. We try to be intentional about our savings first: this is something we should all focus on, but it’s especially important for high-income individuals.

P.S. If you are wondering what that big building is on that island in the featured graphic, that's the Visovac Monastery in Krka National Park in Croatia.