Lifestyle Creep: What Is It And How To Avoid It?

I earn about $130,000 a year. And, lifestyle creep is one of the toughest parts of my life. Here is exactly how I avoid its affects.

My personal goal is to become financially free as soon as possible. As a software engineer in Switzerland, I am earning about $130,000 per year, and, lifestyle creep is one of the toughest parts of my life.

With my salary, I am viewed as a high-income earner. And, people think that earning a high-income makes it easier to become financially free.

And in many ways, it does.

But, most high-income earners are not financially free and a lot of them are not even wealthy.

People believe most high-income earners are wealthy. Indeed they generally show signs of wealth such as a nice car, large house, and pricey suits. But, a lot of these people do not have any savings and accumulate large amounts of debt.

They are not wealthy at all!

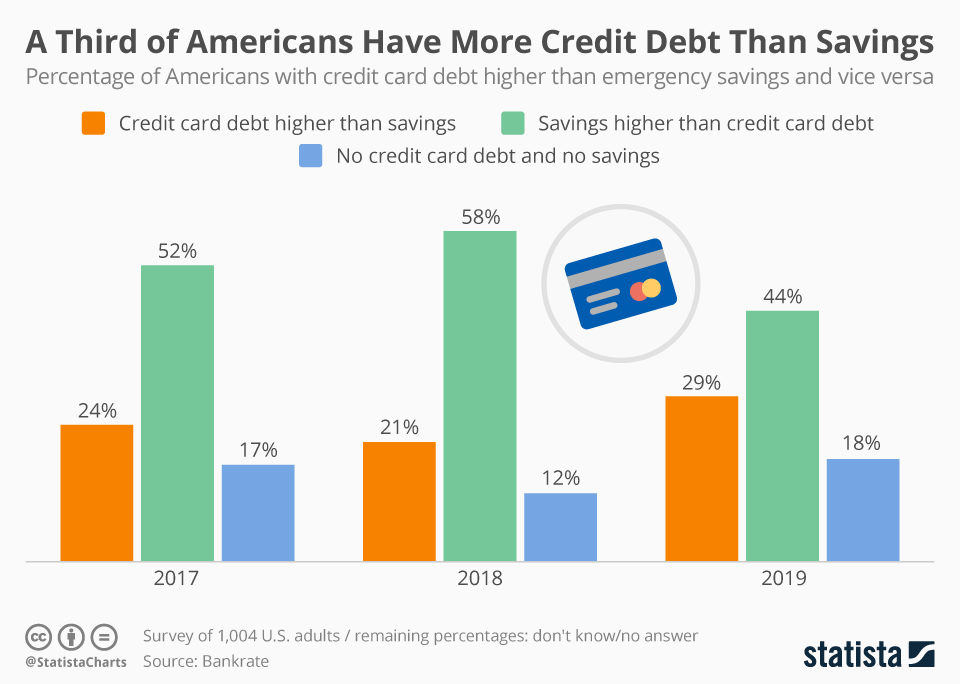

Is it any wonder that a third of all Americans have more credit card debt than savings? It's a scary thought, but it's also true.

The main reason for that is lifestyle creep, and in this post, I'm going to spill the beans about how I battled with the devastating phenomenon as well as how I'm avoiding its grasp!

And more importantly, how high-income earners can overcome lifestyle creep and achieve their own version of financial freedom!

Lifestyle Creep

Let’s start at the beginning: what is lifestyle creep?

As people earn more, they have a tendency to spend more. This means that even though you earn more money each money, you are not saving more. In other words, you aren't acquiring additional wealth. At least, not much.

This is as simple as that. But it has a large impact on their finances.

Lifestyle creep - also known as lifestyle inflation, is the main reason why many high-income earners are not wealthy. In fact, many high-income earners are less wealthy than some low-income earners.

To keep up with their lifestyle, high-income earners are often using credit. They have enough money to pay their bills and their interests each month. But they do not contribute to increasing their net worth.

This is surprising for many people, but when you think about it, it makes perfect sense. If you spend as much as you earn and you buy depreciating assets, your net worth will not grow. You may earn $250,000 per year, but if you spend it all, you are not becoming any wealthier!

Of course, lifestyle creep does not only impact high-income earners. Even a small raise to a low-income earner can turn into an inflated lifestyle. Nevertheless, the more income you get, the more you can inflate your life. And consequently, the worse you can make your situation.

How Lifestyle Creep Affected My Life

My journey into Financial independence started with my own experience with Lifestyle creep.

I have kept a budget since earning my very first dollar.

This is a great thing! Yet, I made one big mistake. I always kept a budget where the total of my budget was also my income. And this is a terrible idea.

At the end of the month, I was always happy if the sum was positive. But, it was almost always negative. I was saving a little money every year. And I was able to invest some money in my retirement accounts.

Once I got my first raise, I simply updated my budget to increase it to my current income level.

And of course, I directly started to spend more.

My big issue was with computers and technology. I am a huge geek. And, I started playing with servers at home. I bought a server rack and started buying and installing servers.

It was a lot of fun, to be honest. At some point, I had 10 systems humming along. I also had a lot of DIY home automation gadgets. At this time, I did not realize what was going on with my finances. After all, my budget was always positive.

At some point, I added tracking of my net worth in my financial dashboard.

And I realized that it was almost not increasing. It came a bit as a shock for me. I was living alone and I had an okay salary that was increasing. So how come I did not have more wealth? I took a look at my expenses over time and I saw that they increasing faster than I ever realized.

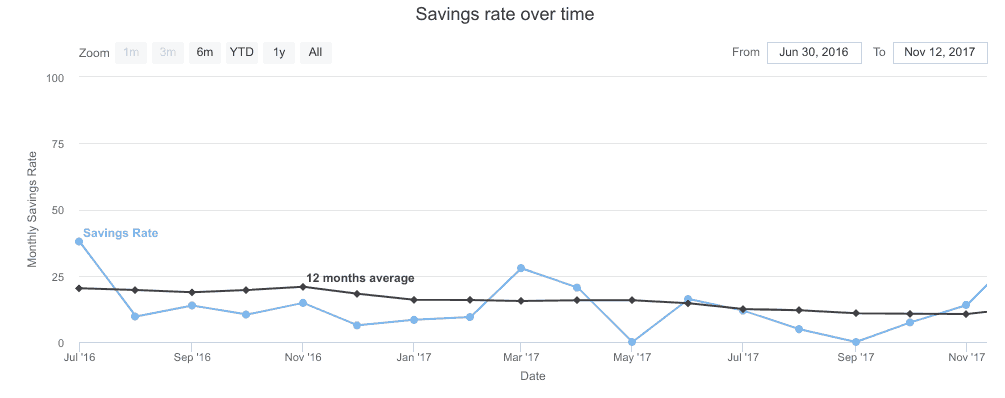

I did some basic research on the internet for ways to make a better budget. And I discovered the concept of savings rate. I added this into my financial dashboard. And I took a look at how it evolved over the years.

Here is my savings rate over time when I did that:

I soon realized something was really wrong. My income increased significantly, yet my savings habits were worse. This was a wake-up call. After this, I decided to seriously cut down my expenses. And I started considering long-term goals.

Fortunately, I never went into debt for lifestyle creep. I paid for everything with cash. And I never went over budget. I never used my savings to sustain my lifestyle. I am considering myself very lucky for that.

Life as a high-income earner

Today, I earn much more than before. But I did not fall into lifestyle inflation (or creep) again. I am saving much more money now. My current average savings rate is almost 50%.

My current income is about $130,000 per year as a software engineer. Even for Switzerland, this is considered as high-income.

Fortunately, I overcame lifestyle creep before I was a high-income earner. Otherwise, I would have wasted a lot more money.

Now that I am a high-income earner, I manage to keep my spending in check. When my earning increases, I simply increase my savings. Every new penny simply goes towards my goals.

Avoid lifestyle creep by using Goals

I think the best tool there is to manage my expenses is to have goals. Before I started being serious with my finances, I did not have financial goals.

Now, I am setting myself goals at the beginning of each year. This helps me a lot during the year. When I get new income, I can simply work towards my goal. I do not think I am loosing out on anything with this. I can see the progression of my goals.

Our current goal is to become financially free as soon as possible. We are not far on the track to Financial Independence. But we are making good progress. We will also probably buy a house during our journey. And children will likely come and change our plans. But I have no doubt that our goals will help us!

Now, not all of the goals have to be aimed towards finances. You can set goals to buy a new TV by the end of the year. Or better, you can set a goal to buy a new car, in cash, in six months. That way, you force yourself to save money towards something you want.

One thing is important: there is nothing wrong with spending money. You are working hard for it. If you want a very good dinner once a week. Then go for it! You need to take each purchasing decision being aware of its impact on your finances. And you need to weight the cons and pros of each spending.

Avoid lifestyle creep by understanding your expenses

There is one thing that is incredibly important and that many people often disregard. You need to understand your expenses.

The first thing you need to do with each expense is to understand how they will impact your goals. This is why your goals are incredibly important. Once you have goals, you need to ask yourself these questions for each expense:

- Will you be able to reach your goals with this expense?

- If not, how much will this put you back?

- Will this expense come back in the future? Is it recurring?

- Will this expense incur some other expenses later on?

- How happier will you be with this expense?

You will see that once you have goals and you ask yourself these questions, you will avoid most expenses.

Avoid lifestyle creep by controlling maintenance

I think that the question that most people ignore is “Will this expense incur some other expenses later on?“. This is more important than you may think.

Indeed, some of your expenses will incur maintenance costs or upkeep costs.

For instance, if you adopt a puppy for $100, you may well spend more than $500 each year to take care of it. You need to think of food, toys and veterinarian fees. Once again, that is not to say you should not buy a puppy if you want one! But there are important things you need to consider when you buy it, not only the purchase price.

Another very good example is when buying a new car. If you upgrade your car, you will also increase your upkeep costs. A bigger car will likely cost you more in insurance. A stronger car will also use more gas and you will spend more to fill it. A better car often also means higher fees for maintenance. Tires will be more expensive as well. These are all the things you need to consider for this expense.

But most people do not care about that. People only think about the purchase price. This could be a great mistake! If you buy several things that then incur a lot of expenses later, you may quickly end up with a lot of extra expenses. And you will wonder how you ended up there!

Avoid lifestyle creep by completely ignoring the Joneses, who are probably flat broke

You probably have heard it many times already, but it is very important! You do not want to try to keep up with the Joneses.

Generally speaking, society expects you to spend more as you earn more. High-income earners are expected to:

- Have a big house

- Have a big car

- Dress very well

- Play golf!

- Have expensive vacations

And this is not an exhaustive list. These expectations have been here for a long time already. You need to fight these expectations for your life. There is no reason you cannot have a high income and a low-end car for instance.

If you ever come to my company parking, it will be easy to spot my car. My car is the cheapest in the parking and by far. My car probably cost twice less than the next cheapest car of my colleagues. And some of these cars are 10 times more expensive than mine. Do I feel any worse because of that? No!

My car never brought me any pleasure. It is just a tool for me. It transports me from A to B every day and does it perfectly fine. I bought it new and I paid for it in cash. I have very low maintenance fees on it. Sure, it is not shiny and nobody will ever waste a sight on it. But it works!

We rent a small apartment and we do not play golf. And all our vacations are kept on a small budget. Do we have a worse time because of that? No!

Because we follow these simple rules with our finances, we can save half of our income every month! This will help us buy a reasonable house in a few years. And this will help us become financially free earlier than if we were trying to do what other people are doing!

High-Income and Financial Freedom

To a lot of people, it seems like earning a high-income helps a lot to become financially free.

It does help, but it is not that simple.

As we saw, high-income earners are not as wealthy as we may think. They are faking wealth and people see them wealthy. But a lot of them will never be able to retire if they want to sustain their lifestyle. And for some of them, retiring would mean cutting in half (or more) their expenses. But you cannot cut half of your expenses and keep the same lifestyle!

Of course, a high-income is not all that bad! But, you need to decide on a certain lifestyle. Once you did that, earning a high-income can help you become financially free. If you are not spending, more income means you are saving more on a monthly basis. This is extremely valuable. Saving more will mean you will be able to become financially free faster!

Conclusion

Simply having a high-income does not make anyone wealthy. And it does not make anyone become Financially Free any faster! Most people with high-income simply spend more than people with less income. It makes sense, right?

Whatever your financial goals are, you need to be cautious with lifestyle creep. It is a trap in which it is very easy to fall into. Everybody should be aware of this trap!

If you are careful with each of your expenses, you can avoid this trap! For this, you will need to set yourself some Financial Goals. What do you want to achieve? This will help you decide which expenses are worth it and which are not.

And you will also need to consider the upkeep costs of your purchases. Most people ignore that and end up with expensive costs from smaller purchases. The direct price of a purchase is sometimes only the tip of the iceberg!

By following these simple rules, we are able to overcome lifestyle inflation ourself. It is not easy of course. Sometimes the temptation is big. But once you consider your real goals, you realize that most expenses will not make you any happier!

What is your experience with lifestyle creep? Did you overcome it? Are you struggling with it?

Frequently Asked Questions

What is lifestyle creep and why should I be concerned about it?

Lifestyle creep, also known as lifestyle inflation, occurs when an individual's discretionary spending increases due to a rise in income. This phenomenon can hinder long-term financial goals, including savings and investments, because as you earn more, you also spend more, often on non-essential items. The main concern is that it can keep you from accumulating wealth and achieving financial freedom, despite a high income.

How can high-income earners overcome lifestyle creep?

High-income earners can overcome lifestyle creep by setting clear financial goals, budgeting meticulously, and being mindful of their spending habits. It's crucial to prioritize savings and investments over unnecessary expenditures. Additionally, understanding the difference between wants and needs, and resisting the urge to match the spending patterns of peers or societal expectations can help maintain financial discipline.

Can setting financial goals really help avoid lifestyle creep?

Yes, setting financial goals is a powerful strategy to avoid lifestyle creep. Goals provide a roadmap for your finances, helping you distinguish between essential and non-essential spending. By focusing on long-term objectives, such as becoming financially free, you can better allocate your resources towards savings and investments, rather than unnecessary lifestyle upgrades.

What role does understanding expenses play in combating lifestyle creep?

Understanding your expenses is crucial in combating lifestyle creep because it allows you to identify where your money is going and make informed decisions about cutting back. Regularly reviewing and categorizing your spending can highlight areas of unnecessary expenditure. This insight enables you to adjust your spending habits in alignment with your financial goals.

How important is it to ignore societal pressures and expectations to avoid lifestyle creep?

Ignoring societal pressures and expectations is incredibly important in avoiding lifestyle creep. Society often equates success with material possessions and an extravagant lifestyle. By focusing on your personal financial goals and what truly brings you happiness, you can resist the temptation to spend excessively on status symbols. Remember, true wealth is not always visible, and financial freedom offers far greater long-term satisfaction than any luxury item.