Keeping up with the Joneses: What Does It Mean?

Are you keeping up with the Joneses? Well, let me tell you why you shouldn't: If the numbers are any guide, Mr. and Mrs. Jones are flat broke.

With few exceptions, most of us aspire to be great people. Successful badasses with lots of money, influence, and purpose. In other words, "the Joneses".

Keeping up with the Joneses Mentality

Keeping up with the Joneses is a kind of mentality by which we try to keep up with our vision for success, and it usually revolves around keeping up with our neighbors. It is the constant interpersonal evaluation of haves and have nots and comparing our material accumulation and visible signs of wealth with our immediate relatives, friends, peers, and neighbors.

More recently, in the era of social media, the Joneses Mentality has grown dramatically with the increased exposure to other peoples’ spending habits and our corresponding increased desire to “keep up.” The idea of not having enough has been among the primary payoffs of most peoples’ social media consumption. This in turn further propels the Joneses Mentality and subsequent unnecessary material consumption. This mentality, in combination with social media, has created an unrelenting vicious cycle of needles spending and debt buildup for many around the world.

What is the Jones Effect?

Let’s take a deeper dive into the Jones Effect so you can better assess whether or not it has taken ahold of you or someone you care about. In my opinion, the Jones Effect is a byproduct of a mild form jealousy and instinctual competition. Say you see your friend wearing a pair of really cool, new Nike shoes that cost over $300. If the Jones Effect takes effect, so to speak, you will be inspired to purchase the same, if not better, versions of the shoes in order to appear on-trend, successful, and wealthy in the eyes of others.

In many ways, we can attribute most of our purchasing behavior to the Jones Effect – being inspired by the people around us or the media is inevitable. However, understanding the pitfalls of the Jones Effect is crucial if your goal is to save money and gain financial independence.

We want to be happy...whatever that happens to mean for you. But, here's the thing: if we aspire to be happy and successful people, why do so many of us try to keep up with the Joneses when many of the Joneses are broke?

Let's face it, the statistics paint a not-so-encouraging picture of the financial landscape in the first world, especially here in the United States.

According to CreditKarma.com, here's what debt is doing to the American population as of June 2017:

Type of debtTotal amountMortgage$8.69 trillionAuto loan$1.19 trillionStudent loan$1.34 trillionCredit card$784 billionTotal household debt$12.84 trillion

To me, this is hard to think about and put into perspective. Though mortgages and student loans are considered by some to be "good debt" (and I don't totally agree), even that amounts to over $10 trillion in debt - debt that is repaid with interest.

5 Effortless Methods to Boost Your Income This Week

If you need extra money, you’ve come to the right spot.

Our team has compiled a list of creative ways you can fatten your bank account this week. Certainly, there’s something here that fits your needs.

This is not a long list, so go ahead and start now, but be sure to bookmark this post so you can easily return later. We’ll keep it updated as offers change or expire.

Keeping up with the Joneses

How did we get into this mess to begin with? According to Credit Karma:

“The rising cost of living, education and medical care have really hit the average American household hard,” said Stephanie Stewart, credit repair researcher at BestCompany.com.

Indeed, the cost of living has been rising — but wages haven’t kept up. As of 2014, median income plummeted by 13 percent from 2004 levels while expenditures increased by nearly 14 percent.

The widening gap between income and expenses looms as a major factor driving American household debt toward unsustainable levels. But that’s just one part of the equation.

Student loan debt is another growing issue that continues to saddle more and more young borrowers, and health costs have skyrocketed too. The Henry J. Kaiser Family Foundation’s 2016 Employer Health Benefits Survey noted that the average health premiums for family coverage have jumped 20 percent since 2011 and a shocking 58 percent since 2006.

Throw all of these factors into a blender and you’ve got a perfect recipe for high American household debt.

The overwhelming majority of the Joneses are in debt

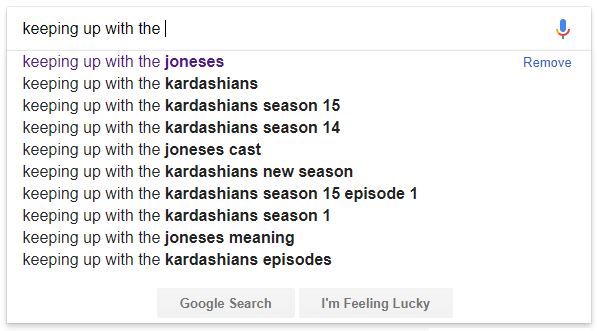

I did a quick "Google Suggest" search for "Keeping up with the", and look how Google completed that sentence based on previous searches:

The first is the Joneses, as you might expect. But the second result is the phrase “Keeping up with the Kardashians”? Really? People want to keep up with the...Kardashians?

I digress...

Here's another shocker set of statistics, this time from the Motley Fool:

It's no secret that America is a nation that runs on debt, but it may surprise you to learn that the overwhelming majority of U.S. adults owe money in some way, shape, or form. According to new data from Comet, here's how many Americans have debt at present:

- 80.9% of baby boomers

- 79.9% of Gen Xers

- 81.5% of millennials

While many Americans owe more in mortgage and student debt than any other type, they also carry credit card, auto, and medical debt, the latter of which is the No. 1 cause of personal bankruptcy filings in the country.

Frankly, the point of this article isn't to prove that we're stupid spenders.

Rather, it is to put into perspective that the Joneses that so many of us aspire to be like are superficial representations of an idea. We don't want to be exactly those people and have to emulate their conspicuous consumption habits - and, we shouldn't, either. We don't even want to be like those people because, according to the data, they are probably in debt.

We want to be happy, and that's good. We want success, and that's also good. We want to build our careers and make a ton of money, then perhaps retire early or at the very least achieve financial freedom and enough FU money to have options in life.

We want that. It's that idea that's desired, not the people who supposedly represent that idea.

We should stop comparing ourselves with the Joneses and stop aspiring to be like other debt-ridden Americans who believe that happiness can be bought like a tube of toothpaste.

Okay okay, I believed this too. I believed that the stuff I had legitimately made me a happier person. Mistakes were made. I understand now that it didn't, but I believed it. I was just as guilty as Mr. and Mrs. Jones. I was there, every day and every night.

Not every job in the gig economy is equal. Here are the best side hustles to consider during your layoff to make the most cash.

Quick tangent: Happiness *can* be bought

This isn't directly on-topic, but close enough. The Joneses believe happiness is bought through the acquisition of stuff. Many also believe precisely the opposite, that happiness can never be bought. The truth, according to one study, might be somewhere in-between, whereby the acquisition of material goods paired with financial peace, allows for general happiness.

Published by Forbes, a dude named Michael Horton ran a clever study that involved giving a person money and asking them to spend it on themselves. Then, each person was given more money, but this time, they had to give that money away instead of spending it on themselves.

Which task made these people happier?

Demonstrably, giving money away made people far happier and more socially connected to people around them. Conversations were started. Surely, a sense of accomplishment was felt by the giver. Knowing that you brought a smile to someone else’s face is a powerful emotion, more powerful than bringing a smile to one’s own face.

Horton divides the source of happiness up into five distinct areas:

- Buy Experiences

- Make it a Treat

- Buy Time

- Pay now, consume later (delayed gratification)

- Invest in others

Without a shadow of a doubt, experiences provide me with more happiness than buying stuff. That helicopter ride I took over the island of Kauai, HI on our honeymoon is an experience that I will never forget. It sure beats the hell out of buying all those miniature model motorcycles that I thought were super cool several years ago.

The less we do more pleasurable things, the more special they become. Dessert feels like a treat to me because I don’t have it at the conclusion of every meal. If I did, it would become “the routine”, nothing special about it…just something that I expect to happen. That’s not happiness.

Time is a critical element of our happiness, and it becomes more and more important the closer we get towards achieving our personal finance goals and calling it quits from work. I want time – time to pursue my hobbies, time to just sit and think, time to enjoy nature. Time is a finite resource, and the better we manage that resource, the happier we tend to be.

I back into spots more often than not. I like the ability to just pull straight out and be on my way when it’s time to go again. Delayed gratification is something that I’ve always naturally done. Maybe that’s why my wife and I have lived so frugally over the past several years to retire early.

And it’s true, I get far more happiness out of life when doing something nice for someone else. I will always remember that time I got a job for someone who was looking for work…far more vividly than any of the jobs that I accepted.

Is this truly the recipe for happiness? Actually, it’s pretty darn close to what I would consider that recipe to include. It’s true, human beings do tend to feel more enjoyment when we do nice things for other people, probably because it makes two people happy instead of just ourselves.

And when it comes to being happy, the more the merrier, right?

Why most people will never get rich

If you used to keep up with the Joneses, you were probably attracted to the idea of being rich and successful. Having stuff to show. A big home. Nice cars.

As we learned from Thomas Stanley's insanely popular book The Millionaire Next Door (<-- affiliate link!), we know that most of this is just for show. These people might earn high incomes, but they aren't rich.

Why?

1: They prioritize other things – The phrase “actions speak louder than words” gets to the heart of this cause. Almost everyone wants riches, but until we prioritize getting rich over spending money on stuff that we don’t need, most of us will never truly accomplish that goal. Most people do not want to get rich bad enough to make it happen, bad enough to cancel expensive cable television services or cell phone plans, or bad enough to drive around in a 10-year old Corolla instead of a brand new Mercedes, or bad enough to say no to expensive dinner or vacation invitations. These are uncomfortable decisions that need to be made to help accomplish financial goals.

2: They don’t believe that they can – In some cases, people simply refuse to believe that anything GOOD could possibly happen to them. Almost as if their lives are composed of a series of misfortunes, similar to the scenarios illustrated of the famous Li’l Abner comic strip. A poor attitude is a devastatingly destructive state of mind for people who want wealth. If we believe that nothing good will ever happen to us, that will ultimately become our reality.

3: They want to keep up with the Joneses – Yep, this point still needs to be included here. When status matters, keeping up with the Joneses is how that status gets maintained. If Jim next door rolls in with a new BMW, guess who wants one too? Most of us see items that we don’t have with at least some degree of jealousy, and this habit is a huge factor in preventing significant wealth accumulation.

4: They don’t accept that “it takes time” – Our inability to delay gratification keeps money flowing out of our wallets faster than we could possibly blink. For most of us, getting rich takes time. It means sacrificing a little discretionary spending for the sake of your future self, and the word “future” scares a lot of people. Life is short, spend money now. What if I die next week in a car accident? I don’t want to wait 10 years before I can enjoy the nicer things in life. These are the excuses that keep us working towards a goal of wealth that never seems to get any closer.

- They think it is too late to start saving – While it is true that the earlier we start saving, the earlier we accomplish our financial goals, that does not mean we can’t start saving in our 30s or 40s. In fact, while I did funnel some money into my 401k throughout my 20s, it was only the bare minimum. I truly started to save BIG MONEY in my early 30s. I started late, but late definitely beats never!

- They built very few passive income streams – Salary is great, but getting rich (and staying rich) becomes much easier when passive income streams are developed as a channel for continuous income. The stock market and real estate investments are passive while commuting into an office and working a full-time job is very, very active. Generating income outside of the office (where your money works for you) is a big factor in getting rich.

- They live on credit – While the use of credit cards is not necessarily a bad thing, using credit to make a purchase before acquiring the funds to pay those purchases off is a huge mitigating factor to getting rich. Arguably, credit card debt is the very worst type of debt in existence. Why? Interest rates are generally through the roof, and running a month-to-month credit card balance may also indicate a tendency to live beyond our means.

If you are reading this blog, then more than likely, your goal isn't to be like the typical person who is living a traditional life. Yup, screw that. You want to live differently.

And, that's good. The majority of the Joneses are broke.

Frequently Asked Questions:

What is "Keeping up with the Joneses" Mentality?

"Keeping up with the Joneses" refers to the mindset where individuals aim to match the societal standards of success and wealth, often equating them with material possessions and visible signs of affluence, such as expensive cars and large houses. This mentality is further amplified by social media, showcasing a constant comparison with others, leading to unnecessary spending and debt.

How does the Jones Effect impact financial behavior?

The Jones Effect, stemming from a form of mild jealousy and competitive instinct, influences people to make purchases based on what they observe in their surroundings or media. This effect can lead to decisions driven by the desire to appear wealthy or successful, affecting one's spending behavior and potentially hindering financial independence goals.

Why do most people not become rich, despite high incomes?

Despite earning high incomes, many individuals don't achieve wealth due to prioritizing spending over saving, a disbelief in their potential for financial success, the allure of keeping up with societal standards of affluence, impatience, late savings start, lack of passive income streams, and reliance on credit. These factors contribute to a cycle of spending that prevents significant wealth accumulation.

Can happiness be bought, and if so, how?

While the purchase of material goods alone doesn't guarantee happiness, spending on experiences, making purchases a special treat, buying time, practicing delayed gratification, and investing in others can contribute to genuine happiness. Experiences tend to provide lasting joy compared to material items, and altruistic spending has been shown to increase happiness and social connection.

What strategies can help avoid the pitfalls of "Keeping up with the Joneses"?

To avoid falling into the trap of "Keeping up with the Joneses," individuals should focus on setting personal financial goals, understanding and controlling their expenses, considering the long-term maintenance costs of purchases, and ignoring societal pressures to display wealth. Developing a mindset of contentment with one's own achievements and financial state, regardless of external comparisons, is key to financial well-being and happiness.