Are you using your new found wealth to watch a ridiculous amount of TV every day?

If you were working 38 years ago and earning the median income, then the amount of money brought in each paycheck would be half of what the median is today (compared to numbers in 2016 USD according to US Census Data).

Wealth in this country continues to grow, and although the wealth gap has increased, the nation as a whole is like Dora from Finding Nemo, but the Duke of Dollars version...just keeps growing, just keeps growing, just keeps growing!

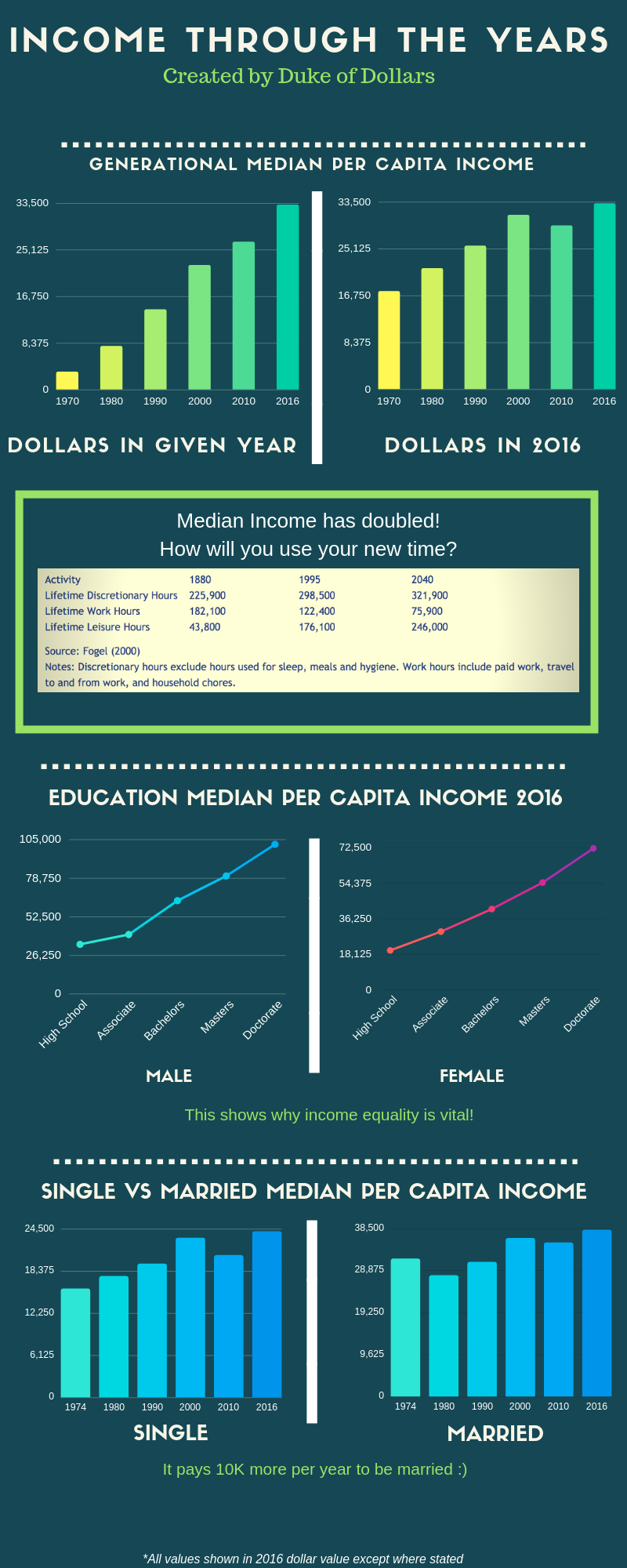

Median Per Capita Income Doubles in 36 Years

If we look at the infographic above, you see that in 1970, per capita income was at $3,100 USD in 1970, or $17,500 in 2016 dollars. Fast forward that to today and you see we're now at a median of $34,000 per person!

This increase in wealth gives you more opportunity to enjoy your life.

The income inequality has grown, and although this post is about income through the years - I don't think Steve would want to have any politics on the blog, so for now I point you to an article by Joshua Kennon to kick start your brain to solve it. Otherwise, let's agree to let it be for now!

Leisure Time Continues to Increase!

Not only do we have more money than they did 38 years ago, we have more time. Now, how in the world can someone have more time? Aren't there only 24 hours in a day?

Fair point.

What I actually mean is this - we have more luxury time (check the infographic to see how we've gone from 43K to 176K leisure hours in our lifetime). Thanks, computer automation...

Just now, I used an electric kettle to boil water in 3 minutes, poured coffee grinds from a ready-made bag bought from the grocery store, and 6 minutes after letting it sit in the French press, here I am enjoying it with my favorite combo of milk and sugar.

Let's go even further! Guess how I obtain my groceries each week?

By grocery shopping online and having them delivered. Yes - delivered. Each Sunday morning while I am snoozing away, somewhere in Amazon land my groceries are being prepped then delivered before 7am, followed by a push notification letting me know once it reaches the door.

This is the current technological state we live in.

We don't have to ride our horse down to the market. Our model-T doesn't have wheels falling off. The steam boat engines aren't roaring in our ears.

I'm not using time each evening to walk down to well for fresh water. Washing machines prevent me from having to use the old school hand washing with a bucket for clean clothes. I'm not writing letters to my family, cousins, nieces, nephews, or friends; I quickly search their name and hit call.

When is the last time you had to look at a map to find a new place? Google Maps has revolutionized how we get from place to place. The list goes on, and on, and on.

I say ALL of that to hammer down the nail into the point for each and every person reading this article. You DO have time in your life.

The Question is How Do You Use Your Time?

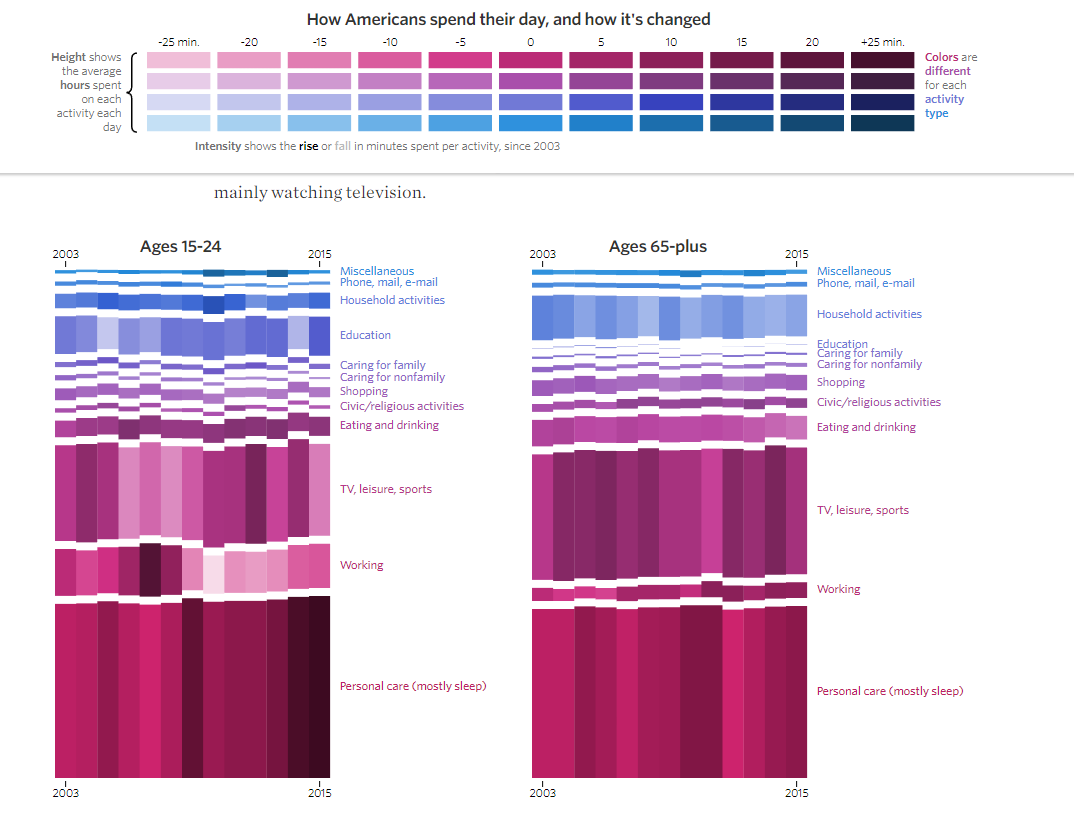

Let's take a quick look!

For those who are ages 15-24, more time is spent sleeping and caring for oneself than any other activity, followed by TV, leisure, and sports.

Some quotes from the Bureau of Labor Statistics

- "Time spent reading for personal interest varied greatly by age. Individuals age 75 and over averaged 51 minutes of reading per day whereas individuals ages 15 to 44 read for an average of 10 minutes or less per day."

- "Watching TV was the leisure activity that occupied the most time (2.8 hours per day), accounting for just over half of all leisure time, on average. The amount of time people spent watching TV varied by age. Those ages 15 to 44 spent the least amount of time watching TV, averaging around 2.0 hours per day, and those ages 65 and over spent the most time watching TV, averaging over 4.0 hours per day."

- "Socializing and communicating, such as visiting with friends or attending or hosting social events, accounted for an average of 39 minutes per day..."

- "Employed adults living in households with no children under age 18 engaged in leisure and sports activities for 4.5 hours per day, 1.2 hours more than employed adults living with a child under age 6."

TLDR;

The most popular leisure activity happens to be watching TV, which accounts for half of our leisure time. On average, we spend at least 2-4 hours per day (depending on your age) being entertained!!

Yes, 2-4 hours PER DAY.

How much is that over a lifetime?

I'm going to use 79 as life expectancy for individuals in the US, start the hour calculation at age 5, use 3 hours per day as the average, count 8 hours as the work/school day, and subtract 8 hours of sleep.

- Life Expectancy: 79 - 5 = 74 years

- Total hours for 74 years= 648,240

- Total hours sleeping in 74 years = 216,080

- Total hours working/schooling in 74 years = 216,080

- This means that after sleep and work, we have a total of 216,080 to use how we want, or in other words, a third of our time in those years.

On average, we are using 81,030 (37% of our remaining) hours watching TV.

Trust me - I love a good movie as much as the next person, but one movie per day on average? The kicker here is this, folks, and one both Steve and I truly agree on:

There is no such a thing as "I don't have time."

It is how you prioritize the time you have. So let me ask you this:

Are you using the worst excuse ever?

I challenge you to never, ever, never ever ever, use the excuse "I don't have time to do X or Y."

Words are powerful.

Instead, rephrase it into "I have a few other things going on." or "thank you for the invite, there are a few things I have to take care of today."

You do have time - you just have more important ways to use it.

Every hour that passes by you become one hour closer to the end of your personal hour-glass. As the one in control of your life and of your time, it's on you to properly decide where to utilize it for maximum happiness. For every single one of us, happiness comes in different forms - if TV makes you happy, then no problem. The choice is yours.

If you are someone who wants to become wealthy, has defined a few goals in your life to achieve or wants to travel the world, then by George get off your couch, turn off the TV, and make it happen, Captain!

Not sure how you want to spend your time? Do the Warren Buffet 5/25 test.

The Best Investment You Can Make

If I told you today that you could put 37K down on a mysterious investment that overtime doubled your income each year for 30 years, allotting you an extra 900,000 over your lifetime based on median per capita income, would you do it? Would you take out a government loan to do so?

What if I asked you a similar question, but instead of an extra 900K in your lifetime, you get to drive a car for the next 10-15 years that systematically depreciates in value - would you do that instead? Or both?

Truly think about it and decide which makes more sense to you. Then ask yourself the following question:

Are We in a Student Loan Crisis or Auto Loan Crisis??

According to Investopedia, the Auto Loan balance in the US has reached 1.22 Trillion USD. Secondly, according to debt.org, the student loan crisis has reached the 1.4 trillion dollar level.

The difference in owning either type of loan has been shown above. Higher level education can truly change the projection of your income throughout your lifetime. As noted in the infographic above, we can compare a few different male median income levels.

- HS = 33K

- Bachelor = 63K

- Masters = 80K

- Doctorate = 101K

Student loan debt hits home for me as I have a little to my name. At first, I was furious with myself for taking on these loans and starting life with an uphill battle. But as I've grown a bit wiser, you can see the census data - those who have a college degree make more money because specialized skills return more money for businesses - aka letting you get paid more!

Degrees definitely matter and should be taken into account when decided what makes sense to you, but there are options to reduce the total cost for your higher education because different career paths do indeed make different salaries - that's where income percentiles can come in handy!

Need help picking a career with a good salary? 50 Highest Paying College Majors.

Is education worth the investment?

By using the median income numbers for the different median income levels for males, we can see that someone graduating college with the average student loan debt of 37,000 can pay off the loan in 10 years with a 6% interest rate.

They will pay a total of $50,000 (12,000 in interest) for that education. But because Billy Bob made that choice to pursue a higher education, he will earn an extra $900,000 in 30 years.

With $30,000, one could live the same lifestyle one currently have AND maxing out all tax advantage retirement accounts with an extra $5,000 leftover for family vacations each year.

Based on this data - and making a good career choice in the degree you choose, the numbers speak for themselves.

Yet, here we are looking at headline after headline about the student loan crisis, people driving their Acuras around town while money flows out of its exhaust pipe every single mile.

Both are a choice, and one we need to take seriously.

These results happen to be different based on your gender, a discussion for another day but worth pointing out just how big the difference demonstrated in the infographic shows. Shaking my head.

We Must Live with the Choices We Make

I was just like many Americans, 18 years old, doing what many people suggested - head to college because higher education is important. Of course, I didn't have the money saved up to pay for it, nor did I have an idea what career it would lead to at that time, or what the student loan terms were. I didn't have any legit plan on how I'd pay them back in the future except "get a good job"...whatever the hell that meant at the time.

Furthermore:

- I didn't apply for scholarships

- I didn't use money from my summer jobs to pay off the debt or tuition the following year

- I used my loan refunds to buy books, pay for clothes and other things not knowing how much wiser it would have been to return the refund instead

- My parents had no idea how student loans worked

- No one offered me a hand or gave guidance on handling the situation in the future

I'm pleading my case fellow, Think Save Retire readers. These are the many defenses on how unjust these loans are, and I have to pay these suckers off years after my college degree arrived at the doorstep.

But no, I will not complain!

I made the decision to sign up for loans, signed my name to the terms they stated, and now must deal with the consequences. That's life.

How am I dealing with the consequences? Paying those suckers off as fast as I can by making the sacrifices required to do so! My Great War of Debt has been going strong and the battle will rage on!

The lesson here is this my friends - read, research, and MAKE the decisions in your life.

You can't let society, your parents, your friends or cousin Bob decide what success looks like or how to achieve it. You must make those decisions based on your own research and decisions, alter course if required, and live with the great results you obtain by doing so!

Concluding Thoughts

This article may feel a bit more ranty on the rant spectrum. These are two important principles (of many) that lead to success in a lifetime:

- Prioritizing your time to maximize happiness and goals

- Make intentional decisions by reading the fine print, researching the topics at hand, and learn from the consequences (good or bad).

With all of your newfound time, you can use more of it productively as you research data points before making big decisions in your life. Doing so allows you to recognize the risks and consequences of those decisions instead of having to go to war with debt in the aftermath instead. :)

Thank you for reading!

The Master Dukes of Dollars are the dynamic duo from The Duke of Dollars Kingdom. The two bloggers held court frequently, delving into lifestyle and personal finance discussions as they searched for ways to live an optimal life, eventually deciding to invite a global audience into their mindsets by establishing their own blog together. Chris is the younger of the two and is in full Great War on Debt mode right after achieving a positive net worth, while Jack – the author of this guest post – is further down the road towards FIRE and is seeking a cure for onemoreyearitis. Their primary mission is to help others build their financial kingdoms, providing the world with a road-map that leads to a fortified personal monetary policy.