Freelancers: 7 Mistakes You Should Avoid When Filing 2019 Self-Employment Tax

If you are a freelancer, your tax situation changes. Prepare for filing your taxes and learn what mistakes to avoid.

If you earn money working for yourself—even if it’s just a side hustle—there are recent tax changes that you need to be aware of.

If this is your first time filing self-employment income taxes, you need to be especially cognizant of the income you report, the rates you pay, and the deductions you claim.

When you work for yourself, even as a part-time freelancer, your tax situation is very different from those who only have W2 income. Failing to understand how this income affects your taxes can drastically increase your odds of an audit—or, worse, foreseen taxes and penalties.

Here are 7 of the most important tax mistakes for freelancers to be aware of for filing 2019 taxes:

Mistake 1. Failing to File 2019 Self-Employment Tax

A lot of people think that income is income and it’s all interchangeable. Wrong! How you make your income matters—especially to Uncle Sam. If you’ve historically worked as an employee for someone else, you’ve probably become used to having your taxes withheld and just figuring out your refund at the end of the year.

But, when you earn a self-employed income that doesn’t come from a full-time job, your tax situation changes. One of the biggest changes is that you have to start paying self-employment tax.

People think that self-employment tax rates are different from normal income tax, which is kinda-sorta true and kinda-sort not. It’s important to understand the difference before you file.

What is Self-Employment Tax?

When you work for another company as a full-time W2 employee, your taxes are typically withheld from your regular paychecks. Not only that, but there are certain taxes—social security and Medicare (FICA) taxes—that your employer is required to pay part of on your behalf.

For example, let’s say you make $100,000 per year. When you get your paycheck, a portion of your earnings will be deducted for federal, state, and local income taxes. You may also have deductions for retirement plan contributions, health insurance premiums, health savings account contributions, etc.

In addition to these deductions, you’ll also have withholding of 7.65% for FICA taxes (Federal Insurance Contributions Act, aka social security and Medicare).

What most people don’t realize is that this 7.65% is actually only half of their FICA taxes. The other 7.65% is paid by their employer.

But, when you’re self-employed or derive income that isn’t covered by a W2, you have to pay the whole 15.3% out of your own pocket.

And that, my friends, is self-employment tax. It’s not an additional tax, per-se. It’s the same tax rate that you pay on W2 income from an employer. It’s just that you don’t have an employer to split it with.

[Note: This is a bit of an over-simplification. Actual FICA rates vary based on the number of dependents you claim, your withholding rate, and other deductions. All of this is typically handled when you complete a W4 as a new employee. But our lawyers told us we need to be careful to avoid writing anything that could be construed as tax advice.]

2019 Self-Employment Tax Rates

The self-employment tax rate for FICA for 2019 is 15.3%. Here’s how it breaks down:

| Tax | W2 Employee Rate | W2 Employer Rate | Self-Employed Rate |

|---|---|---|---|

| Social Security | 6.2% (on the first $132,900 of earnings in 2019) | 6.2% (on the first $132,900 of earnings in 2019) | 15.3% on the first $132,900 of net income plus 2.9% on everything above that |

| Medicare | 1.45% | 1.45% | 2.9% |

| Total FICA | 7.65% | 7.65% | 15.3% |

FICA stands for the Federal Insurance Contributions Act, which is essentially comprised of Social Security (or OASDI: old-age, survivors and disability insurance) and Medicare (also called “hospital insurance tax”).

Basically, when you claim self-employment income on your tax return (whether it’s covered by 1099s or from some other source), TurboTax or any other major tax-filing service will automatically compute your tax liability on that income, after offsetting any expenses, losses, or other deductions. You just have to pay the bill.

Mistake 2. Being Too Liberal With Deductions

One of the most common traps that people fall into—and this applies to everyone, not just side hustlers—is getting too aggressive when claiming tax deductions in order to maximize their refund.

And who wouldn’t, right? Nobody wants to pay more in taxes than they have to.

The problem here is that, when you’re a freelancer or a side-hustler, your taxes are subject to extra scrutiny. The IRS isn’t stupid—its agents realize that when you start freelancing, that makes you a business owner and gives you access to a whole host of new deductions; and for some people, the allure of extra deductions is simply too enticing.

The result: When you start filing a Schedule C or other IRS forms to report profits or losses from independent business activities, your chances of being audited go up. Not a lot, but they do go up.

So, what does this mean for you? It means that you need to take the time to actually study and understand the deductions you’re thinking about claiming BEFORE you claim them. And, you need to be able to document absolutely everything.

If you drove 2 counties over back in March to see a client for your business, you need to know what date you went, what route you traveled, who you saw, and the business purpose for the trip. If you had to buy a new server to store files related to your web development business, you should have a receipt or other documentation of the purpose and also be able to show that you aren’t also using the server to store old family photos.

Lastly, and this really should be obvious: please don’t approximate. Nothing sends up a red flag for the IRS faster than a tax filing covered in round numbers. Why? Because things don’t cost round numbers. A new laptop for your business, with sales tax and shipping, does not cost $1,000. If you use a platform like TurboTax to do your taxes, it will round line items to the nearest dollar, and that’s fine. But don’t guess at expenses or deductions.

Before considering significant tax deductions, such as your business equipment or self-employment income taxes, freelancers should not ignore the potential benefits of understanding Form 1116, which can help in navigating Foreign Tax Credit complexities.

Commonly Misunderstood Deductions

Here are just some of the deductions that people—especially new entrepreneurs—most commonly mess up:

- Start-up costs for starting a business: When you incur costs to start a business,the IRS limits how much you can deduct in start-up costs and organizational costs. You can learn more about these limits through the IRS website.

- Depreciation of work-related equipment: Depreciating certain equipment can be a great way to space out deductions over several years. However, if small business owners go on to sell or lease that equipment, they can incur depreciation recapture. For expensive pieces of equipment that are financed over the course of years, this can lead to tax bills in the tens or even hundreds of thousands of dollars. So be sure you understand recapture before you decide to depreciate business assets.

- Auto payments and maintenance: The IRS treats non-reimbursed business travel very differently than travel using a dedicated business vehicle. But, if you have a business vehicle, there are restrictions for how much that vehicle can be used for personal travel.

- Phone & other utilities: If you use your cell phone for business or work from home, you can deduct a portion of your phone or utility bills as business expenses. However, the percent of the bill you deduct should equal the percent that these utilities are used for business.

There are many additional rules for each of these deductions, along with exemptions and exemptions to the exemptions. If you don’t have time to research what qualifies as a deduction, be sure to speak with an accountant who knows the rules.

Learn more about how NOT to file your taxes as a freelancer.

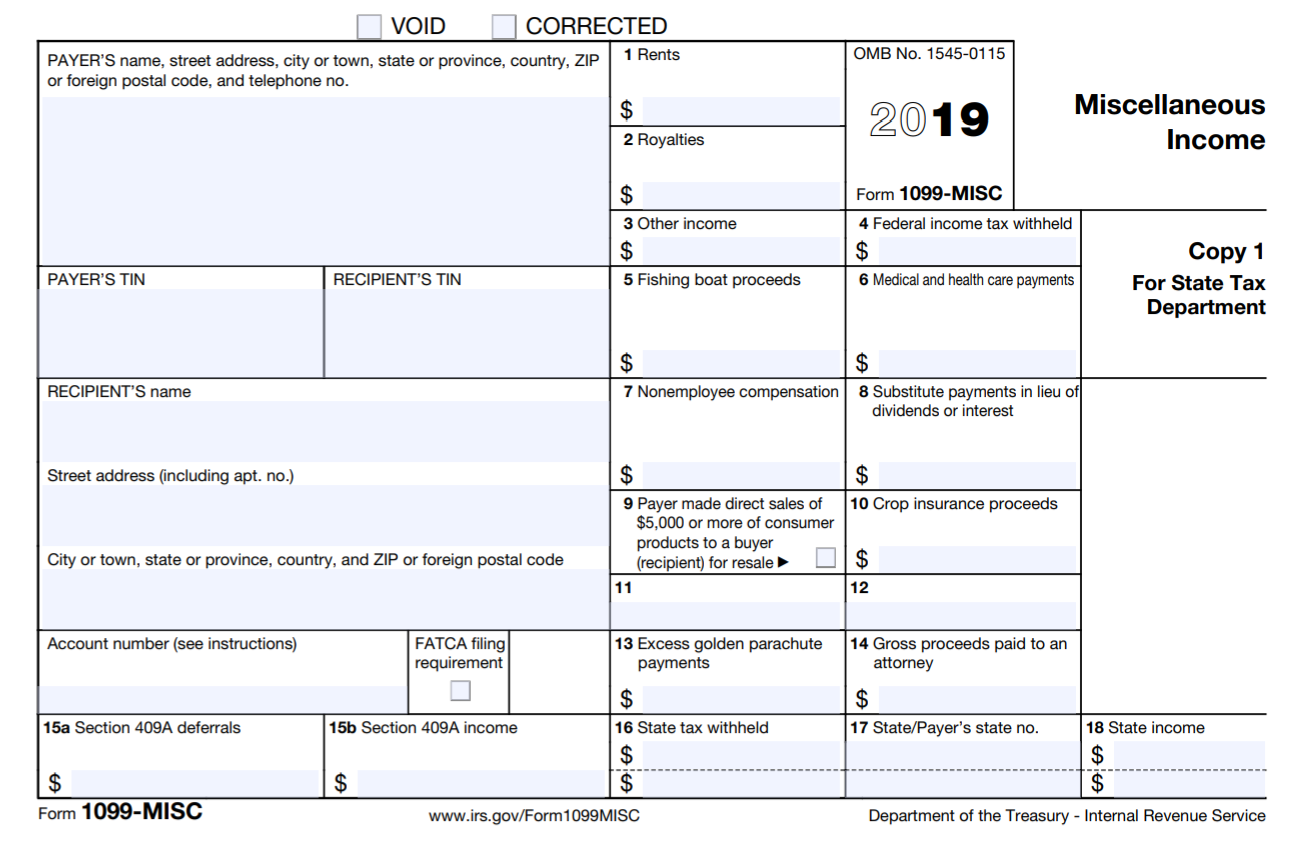

Mistake 3. Not Preparing Self Employed Tax Form 1099s

If you’re going to claim deductions for costs related to legal or professional services, you need to document those costs by issuing 1099s to vendors you pay over $600 in a given year. Failing to issue 1099s when appropriate makes it difficult to document your expenses and may mean you’ll have to skip certain deductions.

Sample 1099

If you need to issue 1099s to lawyers, accountants, or other vendors, you can visit the IRS sample 1099 page for instructions on how and when to complete these documents.

Mistake 4. Skipping the Home Office Deduction

Many entrepreneurs and side-hustlers work from home at least part of the time. It’s a necessary evil when building a business or trying to make extra money.

Some work from home—or at least maintain a home office—precisely because of this deduction.

When you work from home, you may be able to qualify for a home office deduction. This deduction essentially allows you to deduct a portion of your rent, utilities, and other home costs because part of the home is being used for business purposes.

In order to qualify for this deduction, you need to have an area of your home that you use exclusively for business purposes, such as a spare bedroom or an area of a living space.

The home office deduction allows you to deduct a percentage of your home-related expenses equal to the area of your workspace relative to the total square footage of your home.

Let’s say you use a spare bedroom for a home office and let’s say that the bedroom is 12 ft x 12 ft (144 sq ft). And let’s say that your home is 1,500 sq ft total. This would mean that your office is 9.6% of the total square footage of your home, and you would be able to deduct 9.6% of any rent, utilities, or other housing-related expenses as deductible business expenses.

Here again, there are restrictions on how much deduction you can claim and which expenses qualify. For example, mortgage expenses are treated differently than rent. So be sure to do your research or speak with a CPA before claiming this deduction.

Mistake 5. Misunderstanding Non-Reimbursed Mileage

Say it with me: 👏Non👏Reimbursed👏Mileage

Personally, I think this deduction is one of the greatest hidden gems in the tax code for freelancers.

Way back when, company cars were a thing. And the IRS came up with all sorts of rules for how much and what kinds of costs could be deducted for these vehicles.

However, company cars aren’t as common anymore—especially for small business owners and people who are just side-hustling to make extra money.

But, fear not. The IRS also has rules that allow individuals to deduct mileage that they drive each year that isn’t reimbursed by an employer.

The way the IRS has structured this deduction is that there is a single per-mile rate that people can deduct as non-reimbursed mileage expenses. This rate is intended to cover expenses for gas, insurance, tag and title fees, vehicle maintenance—even wear-and-tear or depreciation on your vehicle for each mile traveled.

So, all you have to do is track your mileage for business travel, and at the end of the year, you can deduct the total miles traveled.

And the rate for this deduction? For 2019, the IRS allows individuals to deduct $0.58 per mile for non-reimbursed driving.

Now, keep in mind, this deduction doesn’t apply to normal commutes. So, if you keep an office for your small business or side-hustle, you can’t just deduct every mile driven to or from your office. But this deduction is still super valuable if you regularly travel to meet with clients, purchase supplies, or make deliveries. All you have to do is keep track of the miles you travel for these work-related trips (printing Google Maps routes can be a good way to do this) and remember them when preparing your taxes.

Mistake 6. Payroll Taxes

We’re going to keep this section brief, in part because these laws vary by state and even city. Plus, if you’ve grown a business or side-hustle to the point where you need to hire employees, then you’re probably in a place where you can hire an accountant to help or use a Payroll software like Paycom to help with this.

The important thing to remember is that, as a small business owner, you’re responsible for filing and paying payroll taxes for any employees that you hire.

Even if you only plan on having independent contractors, be sure you do your research to ensure your workers will be properly classified. Companies as big as Uber have run into *a little* trouble with this over the years.

Mistake 7. Filing—and Paying—on Time

Last but not least, one of the biggest—and dumbest—mistakes that entrepreneurs and side-hustlers make related to their taxes is simply failing to file them on time.

Yes, it’s a hassle. And yes, it’s unproductive time. The time you take preparing your taxes is time NOT spent making money.

But you still need to file and pay on time.

If you don’t have time to prepare your taxes, or don’t want to take time away from running your business to prepare them, then work with an accountant who can take care of them for you.

Tax-Filing Extensions

Most people think of “tax day” as April 15th. What many don’t realize is that there’s a second “tax day” that’s 6 months later—on October 15th—and that’s when many small business owners actually file their taxes.

How do they get away with this late filing? By filing for an extension.

The IRS will automatically grant extensions of time for filing your income tax returns if you file Form 4868. However, this form needs to be filed before the normal April 15th deadline.

The extension also only applies to certain documents. For example, filing an extension does not change when you need to send out 1099s. It also doesn’t change anything related to payroll taxes. It only applies to your income tax return.

Quarterly Estimates

Now, this isn’t something that I’ve ever personally used. But, quarterly estimates can be super helpful for side-hustlers or small business owners who need help budgeting for their tax payments throughout the year.

Essentially, what quarterly estimates allow small business owners to do is to approximate their tax liability for a particular quarter and pay toward their anticipated tax bill for that quarter. Then, at the end of the year, they may get some of that money back (or have to come up with more) depending on their final bill.

A lot of people prefer to avoid quarterly estimates—they think of it as paying money before bills are due. And there’s nothing wrong with that unless you’re required by the IRS to pay estimates.

But, if you meet the IRS criteria and are required to pay quarterly estimates, or if you’re worried that you may have a sizable tax bill that you’ll have to come up with all at once, then quarterly estimates may be in your future.

Bottom Line

Whether you’re side-hustling to make extra money or supporting yourself as a fully-fledged entrepreneur, it’s important to understand that your tax situation will be very different than other people who work as full-time employees.

Once you make the switch to self-employment, be sure to research the differences tax code to make sure you understand what you need to file and when along with what deductions you can claim.

If all of this seems like a lot, be sure to speak with a CPA who can help you understand the nuances. These professionals can be well-worth their expertise, especially if they free up your time to continue making money at your small business.